What Is CoastFI? The Simple Math Behind Reaching Financial Independence Without Retiring Early

On this page

- What CoastFI Actually Means

- Why CoastFI Feels So Powerful

- The Core Math Behind CoastFI

- A Simple CoastFI Example

- What CoastFI Changes — and What It Does Not

- The Trade-Off Most People Miss

- The Assumptions People Skip

- 1. Inflation

- 2. Future spending drift

- 3. Return assumptions

- 4. Withdrawal-rate realism

- 5. Sequence risk

- Why CoastFI Is Best Treated as a Milestone

- How to Test Your Own CoastFI Number

- Final Thought

- Next Steps

- 1. Start Free with the FI Architect Web App

- 2. Prefer Owning the Raw Data? Use the Architect-Grade CoastFI Spreadsheet

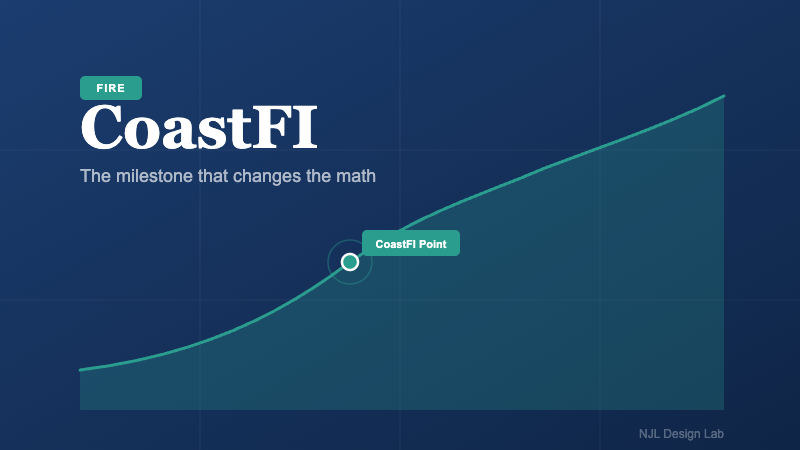

CoastFI is the point where you have already invested enough that, if your money compounds over time, it should grow into the retirement nest egg you need by traditional retirement age — even if you stop making additional retirement contributions today.

That definition is what makes CoastFI so appealing.

It sounds like a release valve for the classic FIRE journey. Instead of sprinting all the way to full financial independence as fast as possible, CoastFI offers a middle milestone: save aggressively early, let time do more of the work later, and use the extra flexibility to design a life that feels better now.

But CoastFI is also easy to misunderstand.

A lot of people hear “I don’t need to save anymore” and translate that into “I’m basically done.” That is where the concept becomes dangerous. CoastFI is not the same thing as full financial independence. It is not a guarantee. And it is not a permission slip to stop thinking critically about your assumptions.

Used well, CoastFI is one of the most useful planning milestones in modern personal finance.

Used poorly, it becomes a spreadsheet fantasy built on assumptions that were never stress-tested.

This article will show you what CoastFI actually means, how the math works, what changes once you reach it, and which assumptions matter most before you rely on it.

What CoastFI Actually Means

At its core, CoastFI means this:

You have enough invested now that, if you leave those investments alone and they compound at a reasonable rate, they should grow into the amount you need for retirement later.

The important word there is later.

CoastFI does not mean you can stop earning money. It means you may be able to stop contributing additional money toward retirement.

That is a major difference.

If you reach CoastFI at 30, 35, or 40, you still need income to cover your current life. Rent or mortgage payments, food, insurance, child care, transportation, travel, and everyday expenses do not disappear. CoastFI simply means your future retirement contributions may no longer be doing the heavy lifting.

That is why CoastFI is best understood as a milestone, not a finish line.

It also helps to distinguish it from a few related ideas:

- Full FI: Your portfolio is large enough today to support your current spending without employment income.

- BaristaFI: You leave or reduce a high-stress job but continue working part-time or in a lower-stress role to help cover current expenses, often with health insurance as part of the equation.

- F-U money: You have enough liquid financial cushion to walk away from a bad situation or buy yourself temporary freedom.

CoastFI sits in a different place.

It says: “My future retirement may already be funded by what I’ve built so far. Now I have more options in the present.”

That optionality is the real attraction.

Why CoastFI Feels So Powerful

For many people, CoastFI is the first version of financial independence that feels psychologically reachable.

A traditional FIRE number can feel overwhelming. A multimillion-dollar target in your 30s or 40s often sounds abstract, distant, or impossible. But a smaller intermediate target — one that relies on compounding over the next 20 to 35 years — can feel concrete enough to act on.

That shift matters.

Instead of asking:

“How do I fully replace my salary right now?”

CoastFI asks:

“How much would I need today so that time and compounding can handle the rest?”

That creates a different emotional experience.

For some people, CoastFI means they can take a lower-stress job. For others, it means they can experiment with entrepreneurship, reduce hours, relocate to a lower-cost city, spend more time with family, or simply stop feeling like every career decision must maximize lifetime earnings.

In that sense, CoastFI is less about retirement and more about pressure relief.

But pressure relief is not the same as certainty.

The more flexibility you want now, the more honest you need to be about the assumptions carrying your plan into the future.

The Core Math Behind CoastFI

The math behind CoastFI is simple in concept, even if the assumptions require care.

You need five inputs:

- Your current invested assets

- Your target retirement age

- Your assumed long-term real return

- Your expected annual retirement spending

- Your retirement withdrawal-rate assumption

Here is the general logic:

- Estimate how much annual spending you want in retirement.

- Convert that spending into a target portfolio size.

- Discount that future target back to today using your assumed rate of return and time horizon.

- The result is your CoastFI number.

The Two-Step Formula

Step 1 — Target Portfolio

Annual Spending ÷ Withdrawal Rate

Example: $80,000 ÷ 0.04 = $2,000,000

Step 2 — CoastFI Number (discount to today)

Target ÷ (1 + r)n

r = real return rate · n = years to retirement

A simple version of the target portfolio formula is:

target retirement portfolio = annual retirement spending / withdrawal rate

If you expect to need $80,000 per year in retirement and you use a 4% withdrawal rule as a rough planning assumption, the implied target portfolio is:

$80,000 / 0.04 = $2,000,000

Then you ask:

“How much would I need invested today for that amount to grow to $2,000,000 by retirement?”

If you assume enough time and a reasonable real return, that present-day number may be much lower than most people expect.

That is the appeal.

But it is also where people get sloppy.

Because once you make this jump from “future target” to “current CoastFI number,” everything depends on the quality of the assumptions underneath it.

A Simple CoastFI Example

Let’s use an illustrative example.

Suppose someone is:

- 30 years old

- planning for retirement at 65

- targeting $80,000 in annual retirement spending

- using a 4% withdrawal assumption

- assuming a 5% real long-term return after inflation

Their target retirement portfolio would be:

$80,000 / 0.04 = $2,000,000

Now we discount that future $2,000,000 back 35 years at a 5% real return.

A rough estimate puts the CoastFI number around the low-to-mid $360,000 range.

That means if they already have roughly that amount invested at 30, and if the assumptions hold reasonably well, they may not need to keep making additional retirement contributions to eventually arrive at the retirement portfolio they want.

That is powerful.

Example at a Glance

~$360K

CoastFI number

at age 30

35 yrs

Of compounding

to retirement

$2M

Target portfolio

at age 65

5% real return · 4% withdrawal rule · $80K/yr retirement spending

It is also only an example.

Change the retirement age, expected spending, return assumption, or withdrawal rate, and the answer changes materially.

That is why CoastFI should never be treated as a single number carved into stone. It is a scenario output.

Useful, yes.

Guaranteed, no.

What CoastFI Changes — and What It Does Not

Once you reach CoastFI, one thing changes dramatically:

You may no longer need to keep saving for retirement at the same intensity.

That can open up real choices.

You might:

- reduce work hours

- take a lower-stress role

- prioritize family time

- spend more now on experiences that matter

- experiment with a new career path

- keep saving anyway, but with less pressure behind it

What does not change is just as important.

CoastFI does not remove the need to:

- earn enough to cover today’s expenses

- manage market risk

- revisit your assumptions over time

- adjust if your spending rises or your return expectations were too optimistic

It also does not mean you must stop saving.

That is one of the most common misunderstandings.

CoastFI is a milestone that gives you options. It is not a rule that says additional saving is now irrational. Some people continue saving because they want more margin. Some want to move their retirement age earlier. Some want to reduce the probability that future adjustments will be necessary.

That is reasonable.

CoastFI should expand your choice set, not narrow it.

The Trade-Off Most People Miss

The hidden trade-off in CoastFI is simple:

More flexibility now usually means more dependence on assumptions later.

If you continue saving aggressively all the way to full FI, you are building a larger margin of safety into the portfolio itself.

If you stop at CoastFI, you are relying more heavily on:

- future compounding

- future market behavior

- future spending discipline

- future retirement age

- future willingness to adjust if needed

That does not make CoastFI bad.

It just means you should talk about it honestly.

The concept works best when the person using it understands that the plan may require future adaptation.

A much better framing than “Will this plan fail?” is:

“If my assumptions weaken, what kind of adjustment would I need to make?”

That is a more realistic planning question.

Maybe the adjustment is small. Maybe you work a little longer. Maybe you continue contributing modestly. Maybe you lower future spending expectations. Maybe you delay the retirement age by a few years.

Those are not catastrophic outcomes. But they are part of the real CoastFI conversation.

The Assumptions People Skip

Most CoastFI errors happen because someone uses clean math with messy assumptions.

These are the big ones to watch.

1. Inflation

If your future spending assumptions are too low, your retirement target will be too low.

And because CoastFI often depends on decades of compounding, even small inflation mistakes can matter.

2. Future spending drift

A lot of people assume their current expenses will remain relatively stable forever.

Sometimes that is true.

Often it is not.

Marriage, children, housing changes, health expenses, geography, aging parents, and lifestyle upgrades can all alter the path.

3. Return assumptions

This is where many CoastFI plans become overconfident.

One spreadsheet set to 8% or 9% is not a law of nature.

Long-term market returns matter, but so does the sequence of those returns, especially when retirement spending eventually begins.

4. Withdrawal-rate realism

The difference between a 4% and 3.5% assumption is not trivial. The difference between a conservative drawdown framework and an aggressive one can reshape the required end portfolio materially.

5. Sequence risk

This matters more once retirement begins than while you are still in the accumulation phase, but it still affects how confidently you should treat your future target.

A retirement plan is not just an accumulation problem. It is also a spending problem.

That is one reason CoastFI should be paired with humility.

Why CoastFI Is Best Treated as a Milestone

The best version of CoastFI is not:

“I never need to think about retirement saving again.”

It is:

“I now have enough progress and enough optionality to make better present-day decisions.”

That is a healthier use of the concept.

Maybe you continue saving, just less aggressively. Maybe you use the milestone to negotiate for a different job. Maybe you spend more on things you genuinely value. Maybe you keep the same career but remove the constant panic that every year off-plan destroys your future.

That is the real advantage.

Used that way, CoastFI becomes a planning milestone that supports better life design.

Used recklessly, it becomes an excuse to stop saving before the underlying assumptions were ever strong enough.

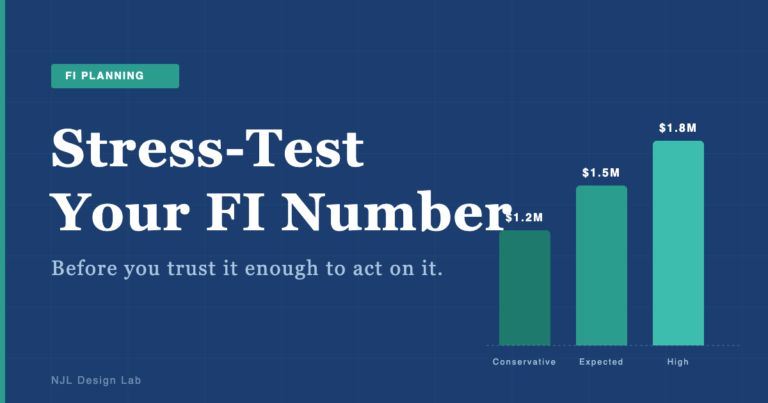

How to Test Your Own CoastFI Number

If you want to use CoastFI intelligently, treat it as a scenario exercise.

Start with this process:

- Estimate what you think retirement spending may look like.

- Build a target portfolio range rather than one single number.

- Test multiple real-return assumptions, not just your favorite one.

- Stress-test different retirement ages.

- Ask what happens if spending rises, returns disappoint, or retirement begins later.

- Decide whether you want more margin before treating CoastFI as actionable.

In other words, do not ask:

“What is my CoastFI number?”

Ask:

“What range of numbers would make me comfortable, and what assumptions would have to hold for each one?”

That is a much better planning mindset.

Final Thought

CoastFI is one of the most useful concepts in the financial independence world because it gives people a middle milestone between endless accumulation and full retirement.

It can reduce pressure. It can create flexibility. It can help you make better career and lifestyle decisions earlier than you thought possible.

But CoastFI is not magic.

It is math, time, and assumptions.

If you understand that, it becomes a powerful tool.

If you forget it, it becomes an attractive story built on fragile projections.

The goal is not to be pessimistic.

The goal is to be clear.

And if CoastFI gives you more options while keeping your assumptions honest, then it is doing exactly what it should.

Next Steps

If CoastFI appeals to you, the worst move you can make is to build your entire plan on a fragile DIY spreadsheet and assume the math will hold forever.

That is how a lot of CoastFI plans quietly fail.

The issue usually is not the idea itself. It is the model underneath it. Weak assumptions, broken formulas, hidden spreadsheet errors, and oversimplified retirement math can make a plan look far safer than it actually is.

So if you want to pressure-test your own CoastFI number, here are the two best ways to do it:

1. Start Free with the FI Architect Web App

If you want the fastest way to run your CoastFI numbers right now, start with the free FI Architect web app.

It gives you a cleaner, more structured way to model your path than a normal spreadsheet, without forcing you to build the logic yourself from scratch. That means you can test assumptions, explore trade-offs, and get a better read on whether your CoastFI plan is actually realistic.

If your goal is to move from vague optimism to a real decision-quality model, this is the best place to start.

Run your numbers free:

https://njldesignlab.com/FIArchitect/index.html

2. Prefer Owning the Raw Data? Use the Architect-Grade CoastFI Spreadsheet

Some people want more than a web app. They want the raw model in their own hands.

If that is you, the Architect-Grade CoastFI Spreadsheet is the better option.

This is not a casual personal-finance worksheet. It is designed as a mathematically rigorous planning model built to eliminate the kinds of hidden errors that make normal spreadsheets unreliable. It is for people who want more visibility, more control, and a stronger modeling foundation than generic templates usually provide.

If you like owning the underlying file, reviewing the logic yourself, and keeping your planning system fully portable, this is the next step.

View the spreadsheet:

FI Architect Spreadsheet on Etsy

The best CoastFI plan is not the one that looks most exciting on a spreadsheet.

It is the one you can still trust after your assumptions are challenged.

If you want to pressure-test your own CoastFI number with a stronger planning foundation, start with the free FI Architect web app or go deeper with the full spreadsheet.