How to Stress-Test Your FI Number Before You Trust It

On this page

- The three assumptions that break first

- 1. Spending baseline

- 2. Withdrawal confidence

- 3. Risk tradeoff logic

- How to stress-test in practice

- Step 1: Build three spending scenarios

- Step 2: Test withdrawal assumptions

- Step 3: Test timing risk

- A worked example

- What you’re looking for

- The mistake most people make

- Why a dedicated tool changes the process

- Go deeper

- The bottom line

FI Planning

Your FI number means nothing if the assumptions underneath it are wrong.

Most people spend weeks calculating a target — then trust it without ever testing it. The math looks precise. The assumptions rarely are.

The question isn’t just “What is my FI number?”

The better question: “Can I trust it enough to act on it?”

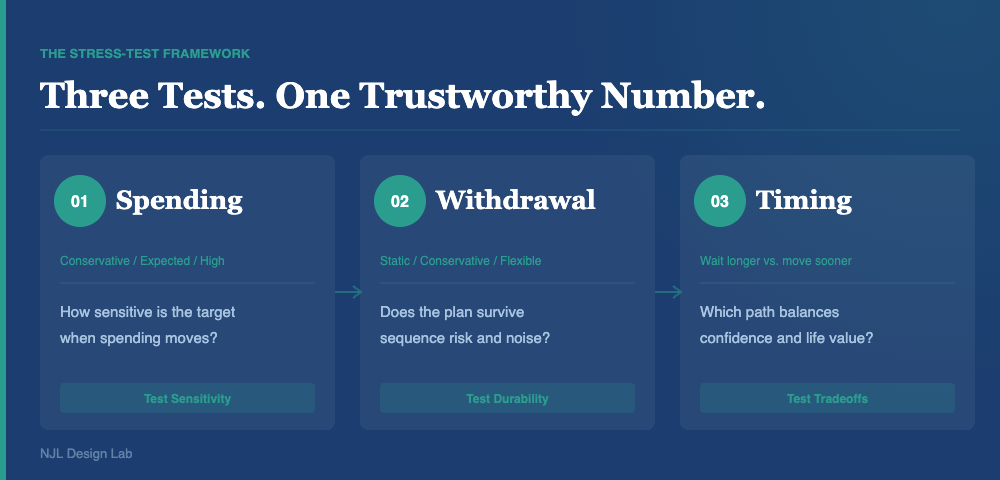

The three assumptions that break first

Most FI estimates rest on three things. If one is weak, the number isn’t ready to use.

- Your spending baseline

- Your withdrawal confidence

- Your risk tradeoff logic

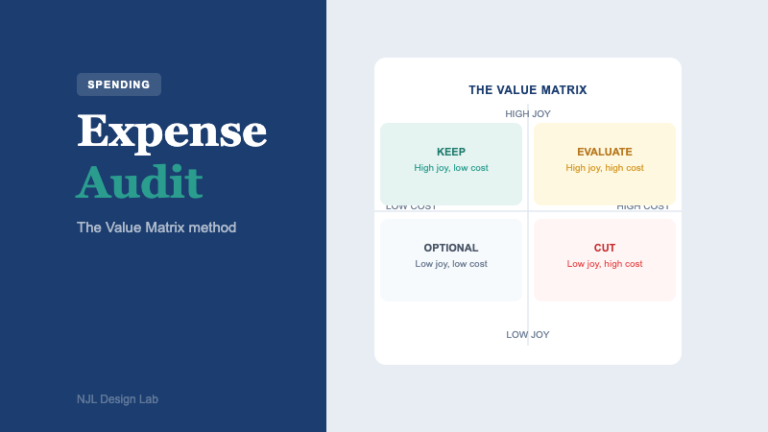

1. Spending baseline

Your FI number starts with what you spend. A fuzzy baseline produces a fuzzy number.

Most people use a rough annual figure — pulled from a budgeting app, a memory estimate, or a best guess. That’s not enough.

Before you can trust the number, you need to answer three things with confidence:

- What you actually spend in a typical month — not what you think, but what the data shows

- Which expenses are genuinely load-bearing to your life and non-negotiable in FI

- Which expenses are variable and could flex without meaningfully changing your quality of life

The goal isn’t a perfect accounting of every dollar. It’s enough clarity to know whether the number you’re targeting is structurally sound.

If your real spend is lower than assumed, your FI target shrinks. If it’s higher, the number is masking a problem. Either way, the baseline has to be tested before you rely on it.

2. Withdrawal confidence

Even a mathematically correct FI target depends on how you’ll draw from the portfolio. That’s where most plans oversimplify.

They pick a static withdrawal rate and move on. Real life doesn’t cooperate.

Spending varies. Returns vary. Taxes vary. Confidence varies.

A robust FI model should answer questions like:

- What if spending runs 10% higher than expected?

- What if I need a cash buffer in year one?

- What if I want to spend more in the early years of FI?

- What if a more conservative withdrawal path makes more sense?

If the number holds across those scenarios, it’s stronger. If it collapses the moment assumptions shift, it’s not ready yet.

3. Risk tradeoff logic

This is the most overlooked assumption — and the most consequential.

People get conservative with money while getting too conservative with life. They delay decisions, experiences, and optionality — all while trying to build the life they want.

That delay has a real cost. That’s a risk too.

Stress-testing your FI number isn’t only about market risk. Ask yourself:

- What is the actual cost of waiting one more year?

- What is the cost of acting one year too early?

- What am I giving up while I try to make the number feel safer?

Sometimes the “safer” financial choice is strategically worse. The number needs context — not just math.

How to stress-test in practice

You don’t need a complex model. You need to stop staring at one output and start testing the assumptions beneath it.

Step 1: Build three spending scenarios

Run your FI calculation with three spending levels:

- Conservative: $48,000/year

- Expected: $60,000/year

- High: $72,000/year

The exact figures matter less than the spread. You’re testing how sensitive your FI target is when spending changes. A fragile plan produces large swings. A durable plan holds across all three.

Step 2: Test withdrawal assumptions

Apply different withdrawal logic to the same spending scenarios. At minimum, compare:

- Static: A simple baseline withdrawal rate, unadjusted for real-world variation

- Conservative: A more cautious rate that accounts for sequence-of-returns risk

- Flexible: A variable spending path that includes a cash buffer in early years

Most FI plans are built on a clean rule that ignores sequence risk, cash buffer logic, and real spending variation. A stronger model shows what happens when the plan has to absorb real-world noise.

Step 3: Test timing risk

Waiting longer may strengthen the number. Moving sooner may reclaim years of your life. Most FI plans never formally model this tradeoff.

Ask yourself:

- What does my FI number look like if I act 12 months earlier than planned?

- What does the gap look like if I wait 12 more months instead?

- Is the difference in portfolio size worth the difference in time?

The question isn’t which path is always better — it’s which path offers the right balance of financial confidence and life value. That’s a decision, not just a calculation.

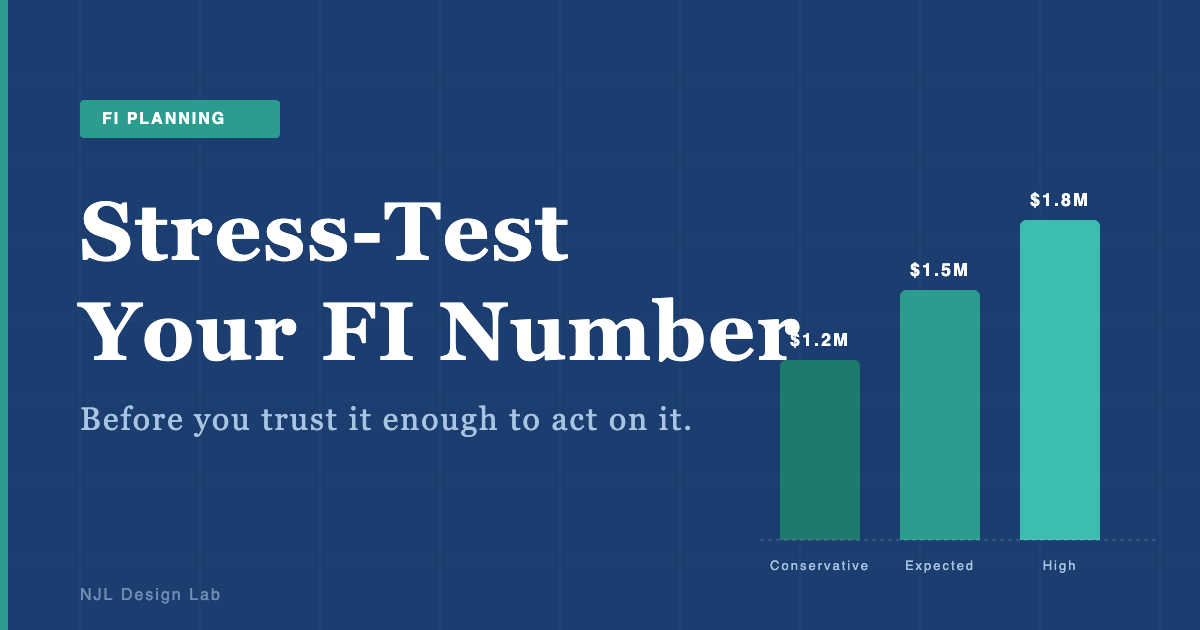

A worked example

Your expected annual spending is $60,000. At a 4% withdrawal assumption, that puts your rough FI target at $1.5 million. Useful as a starting point — but not the end of the analysis.

Now run all three spending scenarios:

- Conservative ($48K/yr): Implied FI target drops to $1.2M

- Expected ($60K/yr): Implied FI target is $1.5M

- High ($72K/yr): Implied FI target rises to $1.8M

That’s a $600,000 spread — before accounting for cash buffers, tax friction, or a more conservative withdrawal path. If your plan only works at the expected scenario, it’s fragile.

The point of the exercise: Your FI number isn’t a single output. It’s a sensitivity check — one that reveals how fragile or durable your plan actually is.

What you’re looking for

The goal isn’t certainty. It’s trust.

A trustworthy FI number survives realistic pressure. It should answer:

- Does this still make sense if my spending is higher than expected?

- Does it hold with a more conservative withdrawal path?

- Does it still work if timing shifts?

- Does the result support a decision I’d actually want to live with?

If yes — the number is useful. If no — keep refining the model.

The mistake most people make

They treat the FI number as a finish line.

It isn’t. It’s a decision input.

A finish line is binary — you either cross it or you don’t. A decision input is contextual. It shifts based on what you assume, how you plan to draw from the portfolio, and what you’re willing to trade off to get there sooner.

A good FI number helps you compare scenarios, surface weak assumptions, and choose what to do next. It shouldn’t be a motivational milestone — it should be a tool you can trust.

Why a dedicated tool changes the process

Once you’re testing multiple scenarios, spreadsheets get fragile fast. It becomes harder to compare assumptions cleanly, easier to miss a variable, and harder to see which input actually moved the result.

That’s where FI Architect was built to help:

- Model spending at conservative, expected, and high levels simultaneously — not one at a time

- Apply different withdrawal rates and see how the FI target shifts in real time

- Identify which assumption is actually driving your number — and which ones barely matter

- Replace a single opaque output with a range of trustworthy, comparable scenarios

Go deeper

The bottom line

The real question isn’t “What is my FI number?”

It’s “Can I trust it enough to act on it?”

If it survives stress-testing, use it. If it doesn’t, keep modeling until it does — then make a better decision with what you’ve built.