How to Do an Expense Audit: The Value Matrix That Turns Spending Into FI Decisions

On this page

- Why Expense Audits Matter

- How to Run a Simple Expense Audit

- Step 1: Export the data

- Step 2: Categorize the spending

- Step 3: Mark irregular expenses

- Step 4: Build the baseline

- The Value Matrix — Turning Data Into Decisions

- High joy, low cost

- High joy, high cost

- Low joy, low cost

- Low joy, high cost

- Applying the Matrix to Real Spending

- Edge Cases That Need Honest Treatment

- Should taxes count?

- Should debt principal count?

- What about irregular events?

- What about behavior change?

- Why This Matters for Financial Independence

- The Audit → Matrix → FI Loop

- Conclusion

Most people track spending, but few understand it.

That gap matters more than it seems. You can log transactions, review statements, and still have a weak grasp of what your life actually costs, which expenses deserve protection, and which ones are quietly making your FI plan heavier than it needs to be.

An expense audit is a structured review of your real spending over a defined period. The goal is not restriction. The goal is clarity.

The Value Matrix is what makes that clarity useful. It turns raw spending data into a decision system. Instead of asking whether you should spend less in general, it helps you decide what to keep, what to optimize, and what to cut.

This article gives you a repeatable method. You will leave with a clear audit process, a practical decision framework, and a cleaner way to connect spending choices to financial independence.

Traditional budgeting often fails because it starts with rules before it establishes reality. An expense audit reverses that order. First measure. Then decide.

Why Expense Audits Matter

For FI planning, spending is not just a monthly behavior. It is a structural input.

Your spending affects how much you can invest now. It also affects how large your future portfolio needs to be. If that baseline is fuzzy, your FI number is fuzzy too.

This is why spending clarity has leverage. A cleaner view of recurring costs, irregular costs, and low-value defaults gives you a more accurate savings plan and a more accurate target.

Even small recurring changes matter.

If you reduce spending by $250 per month, that is $3,000 per year. Under a simple 4% withdrawal assumption, that implies roughly $75,000 less portfolio required to support the same lifestyle. The monthly change looks small. The FI impact is not.

FI Impact Example

$100/month reduction = $1,200/year = ~$30,000 less needed at 4% withdrawal rate

$250/month reduction = $3,000/year = ~$75,000 less needed at 4%

$500/month reduction = $6,000/year = ~$150,000 less needed at 4%

The deeper benefit is not only lower spending. It is better spending.

An expense audit helps you separate categories that genuinely improve life from categories that survive only because they were never challenged. That distinction is more useful than generic frugality.

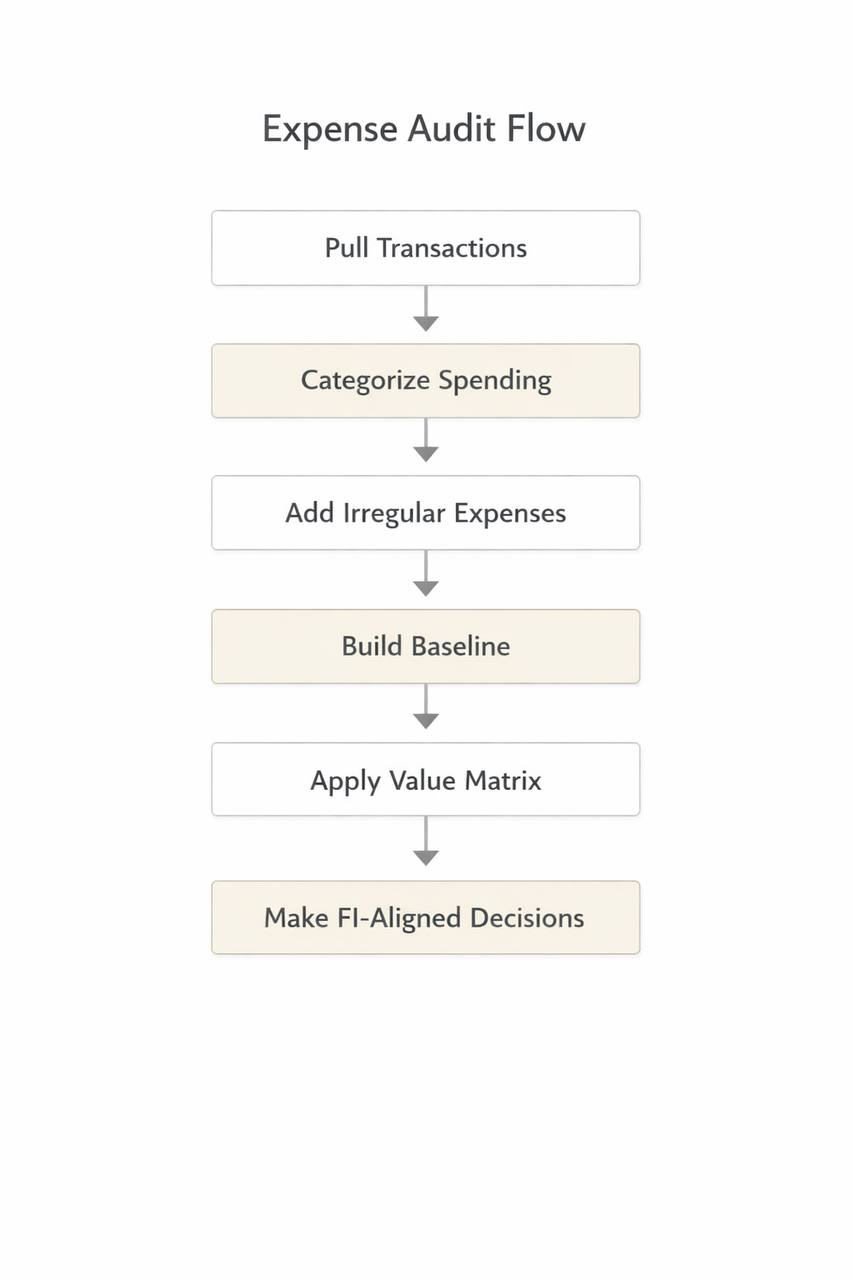

How to Run a Simple Expense Audit

Use a short, deterministic process.

Step 1: Export the data

Pull the last two to three months of transactions from:

- checking accounts

- credit cards

- debit accounts

- any shared household spending accounts

Use whatever tool gives you clean exports fastest. Bank CSV exports work. A spreadsheet works. A budgeting or expense-tracking app also works if the data is accurate and complete.

Step 2: Categorize the spending

Group every transaction into broad categories first.

Start with categories such as:

- housing

- groceries

- dining out

- transportation

- insurance

- childcare

- travel

- subscriptions

- health

- entertainment

- miscellaneous

Do not over-design the category system on the first pass. The goal is usable signal, not taxonomy perfection.

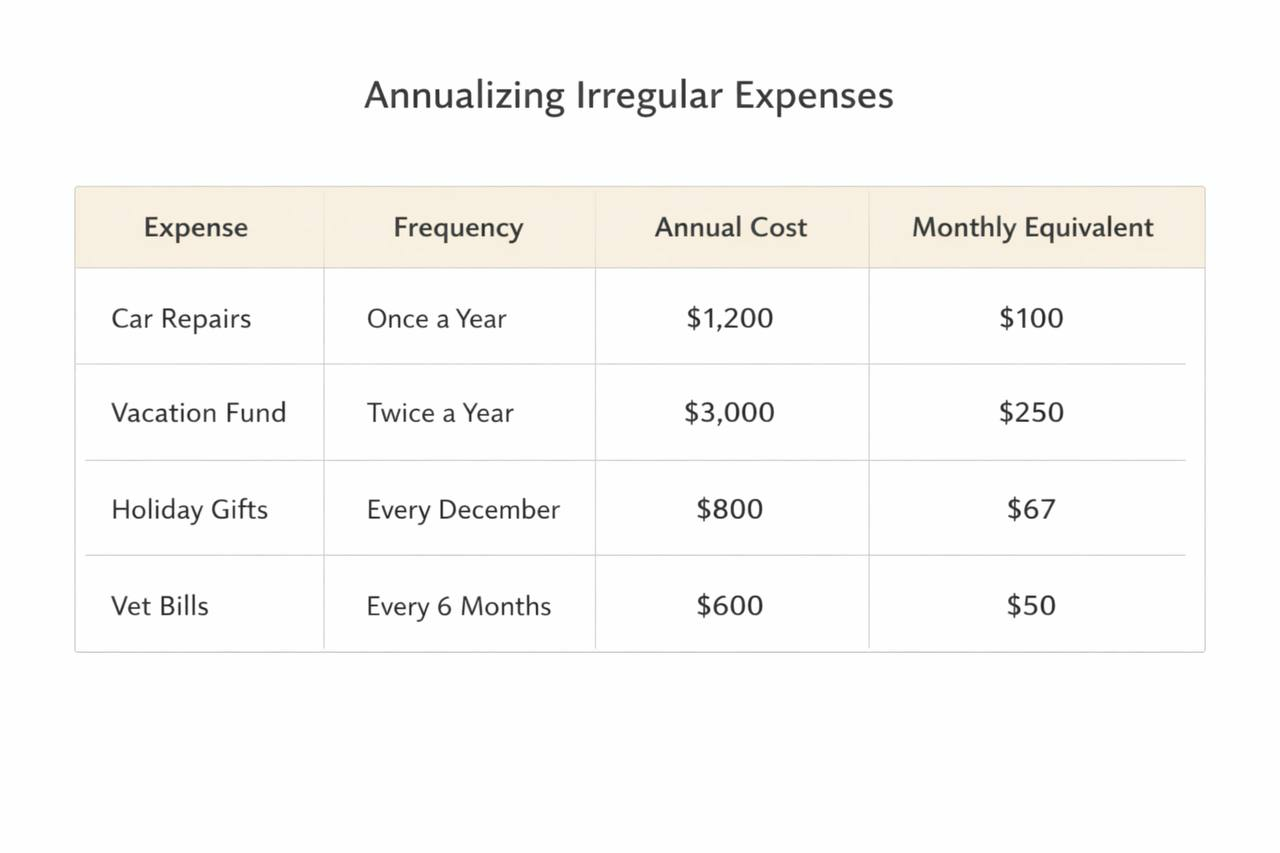

Step 3: Mark irregular expenses

Flag expenses that do not appear every month but still belong to the real cost of life.

Irregular expenses include items such as:

- annual insurance premiums

- property taxes

- medical spikes

- home repairs

- school costs

- gifts

- travel bursts

- maintenance events

If they are real, include them. Do not let timing hide them.

Step 4: Build the baseline

Calculate what your life actually costs in a normal year.

Average variable spending where appropriate. Annualize irregular items. Then combine those numbers into a working baseline.

At this stage, do not optimize yet. Just answer these questions:

- What does this household actually spend?

- Which categories are larger than expected?

- Which categories are fixed versus adjustable?

- Which categories appear to be drifting upward?

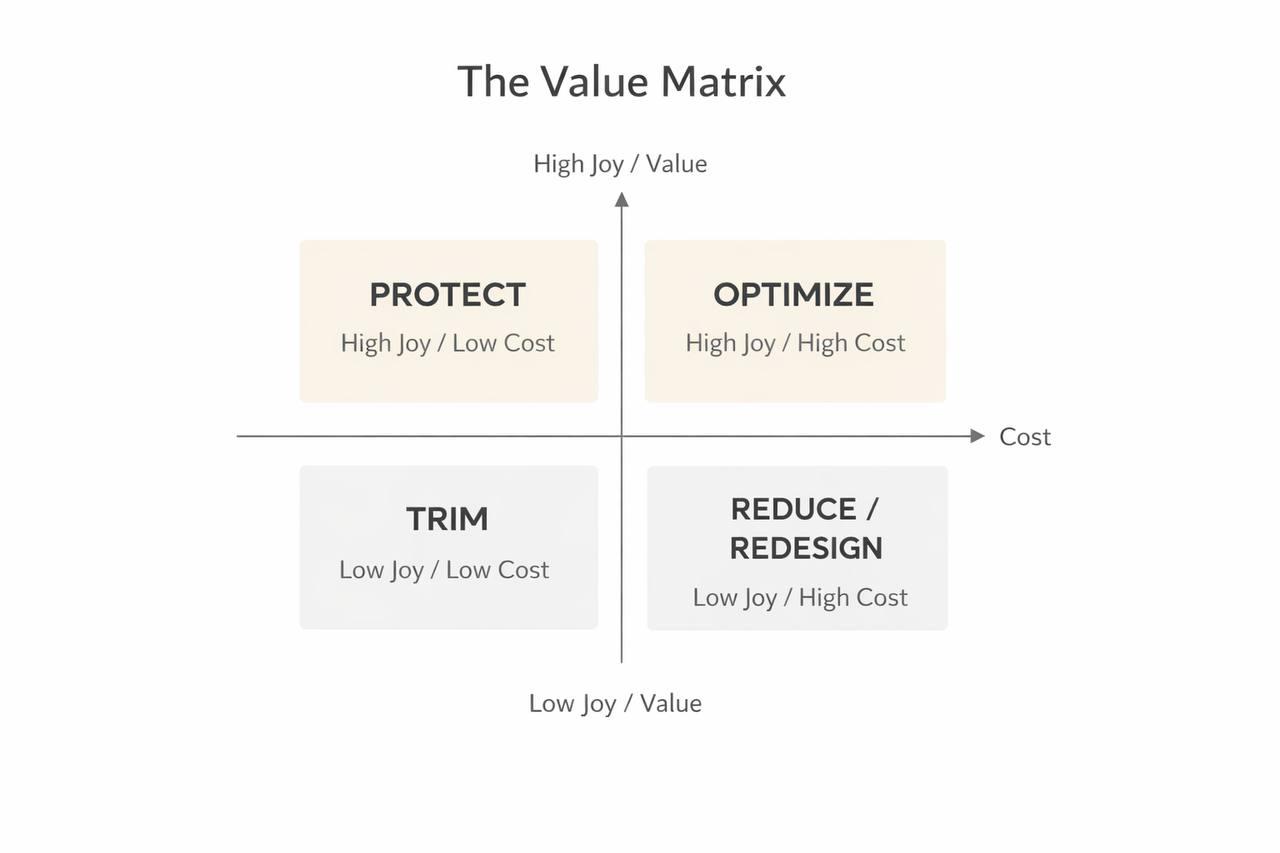

The Value Matrix — Turning Data Into Decisions

Once the audit is complete, the next step is not “cut everything.” The next step is classification.

The Value Matrix is a decision filter, not a budget.

It evaluates spending on two axes:

- value or joy to your life

- cost to your plan

That creates four quadrants.

High joy, low cost

Decision logic: protect it.

These are categories that create meaningful value without materially stressing the plan.

Examples:

- a low-cost hobby you use every week

- a subscription that saves real time and friction

High joy, high cost

Decision logic: optimize it.

These categories may deserve to stay, but they should earn their cost.

Examples:

- housing in a location you deeply value

- travel that meaningfully improves your life but needs tighter structure

Low joy, low cost

Decision logic: remove or minimize it.

These costs look harmless in isolation, which is why they often survive too long.

Examples:

- forgotten subscriptions

- recurring convenience purchases you barely notice

Low joy, high cost

Decision logic: fix this first.

These are the clearest drags on the FI plan because they combine weak value with real financial weight.

Examples:

- an expensive commuting setup you dislike

- a premium service or membership that adds little value

Protect: High joy, low cost Optimize: High joy, high cost Trim: Low joy, low cost Reduce/Redesign: Low joy, high cost

The point is not to moralize spending. The point is to create a better filter for decisions.

Applying the Matrix to Real Spending

Once your spending is categorized, the matrix reveals patterns.

That is when the exercise becomes useful.

Take a few real categories and place them deliberately.

Groceries might land in high joy, low cost if home cooking supports health, routine, and lower total spend. Dining out might land in high joy, high cost if it is meaningful socially but still worth optimizing. A stack of unused subscriptions may land in low joy, low cost. A costly housing or commuting arrangement that adds stress may land in low joy, high cost.

This is also where emotional spending and functional spending diverge.

Functional spending solves a real need. Emotional spending often solves fatigue, status pressure, boredom, or convenience stress. That does not automatically make it bad. But it should make you inspect it more carefully.

The matrix helps expose whether a category is supporting the life you want or compensating for a system that is already under strain.

Edge Cases That Need Honest Treatment

A good expense audit becomes more useful when the messy categories are handled directly.

Should taxes count?

In many cases, yes, because taxes are part of the real cost of life.

But they should be labeled clearly. Taxes are structurally different from discretionary consumption. The mistake is not including them. The mistake is mixing them carelessly with adjustable categories.

Should debt principal count?

That depends on the purpose of the analysis.

If you are measuring pure cash outflow, principal payments matter because cash leaves your account. If you are isolating pure consumption, principal is different because it also builds equity.

The important thing is consistency.

What about irregular events?

Annualization prevents you from understating your life.

If a real cost appears once or twice per year, ignoring it makes the monthly picture look cleaner than reality. Annualizing those expenses gives you a more truthful planning number.

People commonly forget:

- insurance renewals

- medical or dental spikes

- home maintenance

- travel bursts

- tax-related payments

- gifting seasons

What about behavior change?

Awareness alone is not a system.

A spending category driven by exhaustion, chaos, or social pressure may not improve just because you noticed it. The audit shows the pattern. The fix may still require operational changes, habit changes, or environment changes.

Why This Matters for Financial Independence

FI is driven by two simple variables: how much you need and how much you can save.

That is why spending clarity matters so much. It improves both.

A basic FI framework often starts with the 4% rule. In rough planning terms, that means you estimate annual spending in retirement and multiply by 25 to get a target portfolio size.

That framework is only as good as the spending number you feed into it.

If your annual spending estimate is overstated because of drift, leaks, or unexamined defaults, your FI target rises. If your spending estimate is cleaner and lower without reducing real quality of life, your FI target falls.

FI Impact Example

$100/month reduction = $1,200/year = ~$30,000 less needed at 4% withdrawal rate

$250/month reduction = $3,000/year = ~$75,000 less needed at 4%

$500/month reduction = $6,000/year = ~$150,000 less needed at 4%

An expense audit therefore does more than trim categories. It sharpens the denominator of the entire plan.

The Audit → Matrix → FI Loop

The most useful version of this process is not one-time. It is repeatable.

The loop is simple:

- Audit the real spending.

- Classify it with the matrix.

- Adjust the FI plan using the cleaner baseline.

- Repeat on an annual or semiannual cadence.

That loop helps prevent lifestyle creep because it forces recurring review. Categories that once felt harmless get re-tested. High-value spending gets protected intentionally instead of accidentally. Low-value drift gets caught earlier.

The Audit → Matrix → FI Loop

Expense Audit

↓ Clear Baseline

↓ Value Matrix

↓ Better Decisions

↓ More Accurate FI Number

↓ Less Drift, More Alignment

↓ Repeat Annually

Over time, this creates a stronger financial operating system. You stop reacting to spending emotionally and start evaluating it structurally.

Conclusion

The real benefit of an expense audit is not a prettier spreadsheet.

It is clarity.

Clarity gives you control. Control improves the quality of your decisions. Better decisions reduce drag in the plan and make FI progress more deliberate.

That is the sequence worth keeping: clarity -> control -> FI acceleration.

If you want a practical starting point, run your first audit this week.

Pull two to three months of transactions. Build the baseline. Mark irregular expenses. Then run every meaningful category through the Value Matrix.

If you want a simple place to keep that work organized afterward, a budgeting and net-worth tracker like Money Map Budget Tracker can help turn a one-time audit into an ongoing review system.

First get clear. Then decide. Then optimize the plan with better evidence.