The Real Work in FI Is Not the Number. It’s the Control Loop.

On this page

- Why the number is not enough

- What a control loop actually does

- What the loop reveals

- Why this creates optionality

- A simple FI control loop

- 1. Review the system honestly

- 2. Separate fixed from variable

- 3. Identify recurring drift

- 4. Check value, not just cost

- 5. Make one or two adjustments

- What this looks like in real life

- What not to do

- The real reward

- Go Deeper

- How to keep the loop alive

Financial independence works better as a system you keep steering than as a number you hope will save you.

Financial independence is often sold as a finish line.

Most people treat FI like a math problem. But math doesn’t maintain itself.

Hit the number. Cross the threshold. Turn the engine off.

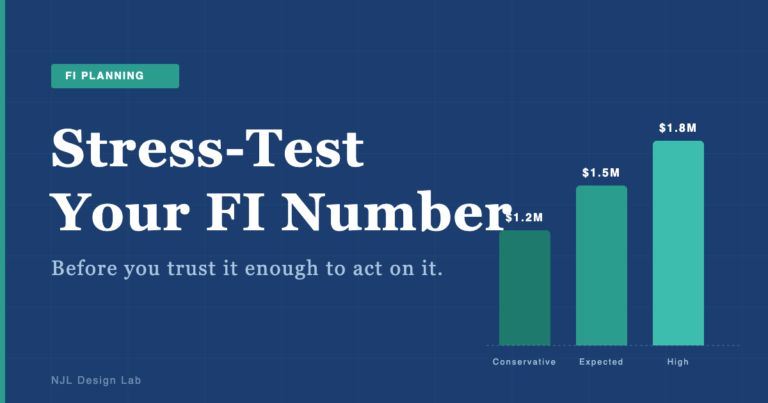

That framing is useful up to a point. You do need a target. You do need a working estimate of what life costs, what your assets can support, and how much margin you have built.

But the number is not the whole job.

The deeper work is building a control loop that keeps your financial system honest over time.

A control loop is what helps you notice drift before it becomes damage. It is what catches leaks before they become a pattern. It is what turns FI from a one-time milestone into a durable operating rhythm.

That is where the real progress lives.

Why the number is not enough

A good FI number gives you direction.

What it does not give you is maintenance.

It does not tell you whether spending has drifted upward. It does not tell you whether your household priorities changed. It does not tell you whether the tradeoffs that made sense eighteen months ago still make sense now.

A clean FI number without a review system is a snapshot.

A control loop is the movie.

That difference matters because life is not flat.

Expenses move. Income changes. Family needs shift. Energy changes. Time pressure changes. A system that looked efficient two years ago can quietly become bloated, stale, or misaligned.

If you only track the destination, you can miss the drift.

If you run a control loop, you can correct it while the stakes are still small.

So if the number can’t keep you honest, something else has to.

What a control loop actually does

A control loop is just a repeatable way to inspect the system and make small corrections before problems compound.

In practice, that means you are not trying to micromanage every dollar every day. You are creating a rhythm that helps you answer a few essential questions:

- What changed?

- Where did drift show up?

- What is still working?

- What no longer deserves a place in the system?

- What deserves more attention because it creates real value?

This is the maintenance layer most people skip.

They focus on the big target and ignore the operating rhythm underneath it. But FI is not maintained by motivation. It is maintained by visibility, repetition, and course correction.

The control loop is not about perfect budgeting. It is about staying in contact with reality long enough to protect optionality.

An expense audit can be one useful snapshot inside the loop.

This article is about the operating rhythm itself.

The deeper value is the recurring rhythm that tells you when to look again, what changed, and where to make the next small correction.

What the loop reveals

Once you review your financial system regularly, a few things become easier to see.

First, you see the fixed pieces.

Some costs are simply part of the life you are choosing right now. Housing, insurance, childcare, debt obligations, or other core commitments do not need to be re-litigated every week. Once they are understood, they can be carried forward with less noise.

Second, you see the variable pieces.

This is where the real opportunity usually lives. Drift tends to hide in recurring subscriptions, convenience spending, friction spending, emotional spending, and small defaults that no longer earn their keep.

No single line item looks dramatic.

But together, they can move the whole system.

Third, you see value more clearly.

Not everything should be cut. Not everything should be optimized away. Some spending genuinely improves your life, your family, your energy, or your time.

The point is not austerity.

The point is discernment.

The loop helps you separate:

- what is essential

- what is genuinely valuable

- what is merely habitual

- what is expensive and low value

That distinction is where calm begins.

Why this creates optionality

Optionality is the real payoff.

Not just a lower number. Not just a cleaner spreadsheet. Not just a better estimate.

Optionality.

When you know what your system actually costs, you gain flexibility. You can redirect money faster. You can keep what is working on purpose. You can spot waste sooner. You can make better tradeoffs because you are not guessing.

Optionality changes the emotional texture of FI.

Without it, FI can feel like a future promise. With it, FI becomes a present capability.

You are not waiting for life to begin after the number. You are already practicing the skills that make life more stable now.

That is why the loop matters more than the milestone itself. The milestone is useful, but the loop is what keeps the milestone meaningful after you reach it.

A simple FI control loop

You do not need a complicated framework.

You need a cadence.

For most people, a quarterly review is enough. An annual deep review can sit underneath it. The exact schedule matters less than the consistency.

A practical control loop looks like this:

1. Review the system honestly

Look at what came in, what went out, and what repeated.

Do not aim for perfect categorization. Aim for accuracy that is good enough to support a decision.

2. Separate fixed from variable

Lock in the obvious commitments first. Then focus attention on the flexible areas where change is actually possible.

3. Identify recurring drift

Look for spending that keeps showing up without creating enough value to justify its place.

Do not overreact to one strange month. Look for patterns.

4. Check value, not just cost

Some categories should stay because they matter. Others should shrink because they are expensive without enough return.

The question is not always, “Can I cut this?”

Sometimes the better question is, “Should this still be here at all?”

5. Make one or two adjustments

This is the critical step.

The goal is not to redesign your whole life in one sitting. The goal is to improve the system enough that the next review starts from a better place.

Small corrections compound.

That is the game.

What this looks like in real life

The loop in one sentence: “Look regularly, adjust lightly, repeat forever.”

Imagine a household that does a 30-minute review at the end of each quarter.

Nothing dramatic happened. Income is stable. The big bills are familiar. At first glance, everything looks fine.

Then the review catches two quiet shifts:

- delivery spending keeps creeping up during overloaded weeks

- one support expense still costs real money, but is clearly worth keeping because it reliably reduces family friction

That review does not lead to a life overhaul.

It leads to two small decisions:

- put a simple guardrail around delivery spending next quarter

- keep the support expense on purpose instead of treating it like a budgeting failure

That is a control loop.

Not punishment. Not purity. Not spreadsheet theater.

Just enough visibility to catch drift, protect what matters, and make the next quarter slightly stronger than the last one.

Another common pattern: childcare costs drop as kids age, but lifestyle creep quietly fills the gap. The budget technically improves, yet the household feels no freer because the loop never caught the drift.

What not to do

Do not turn the process into punishment.

If the review becomes a moral trial, people avoid it. If it becomes a deprivation ritual, the system collapses. If it becomes too detailed, too tedious, or too self-critical, it stops working.

Also do not confuse clarity with austerity.

The goal is not to strip life down to the bone. The goal is to remove noise so the parts that matter can stand out.

And do not make the mistake of thinking one clean year means the work is done.

It is not done.

That is the point.

The loop exists because life changes. Priorities evolve. Systems drift.

Durability comes from returning to the review, not from getting it perfect once.

The real reward

The reward is not just better numbers.

It is better judgment.

It is the feeling that your financial life is being managed instead of merely endured. It is knowing where your money is going. It is knowing what deserves to stay. It is knowing what no longer fits.

Most of all, it is knowing that FI is not a freeze frame.

It is a living system you can keep steering.

That is what makes the control loop so powerful.

It gives you a way to keep the gains you already earned. It gives you a way to protect optionality. It gives you a way to compound calm.

In the long run, that matters more than the number itself.

Go Deeper

If you want to keep building this layer of your FI system, these are the most relevant next reads:

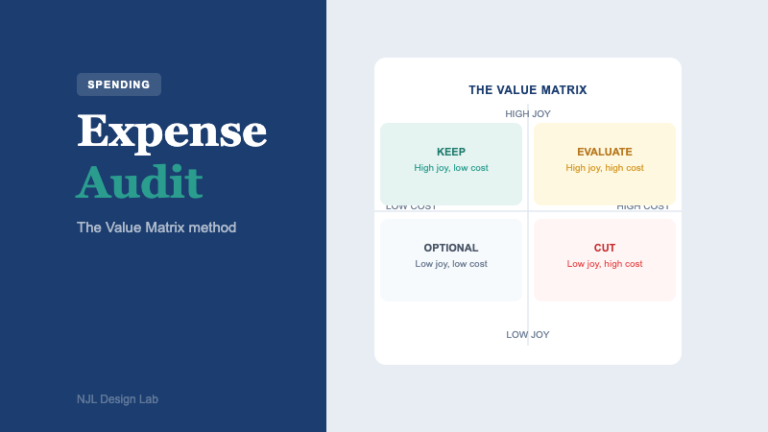

- How to Do an Expense Audit: The Value Matrix That Turns Spending Into FI Decisions

- The Boring Middle of Financial Independence Isn’t Boring. It’s Identity Work.

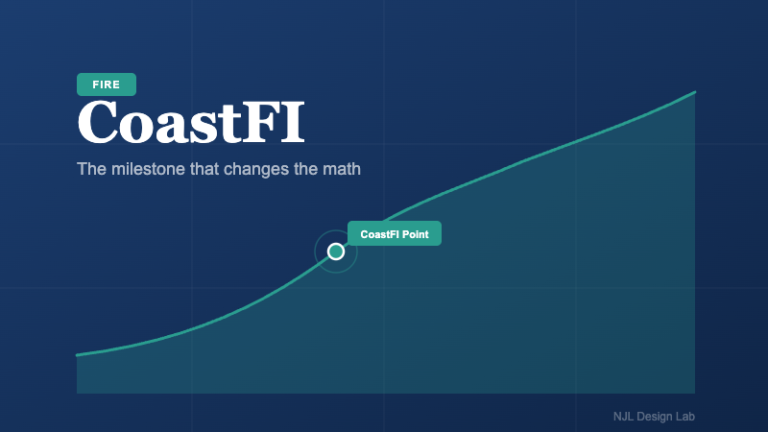

- What Is CoastFI? The Simple Math Behind Reaching Financial Independence Without Retiring Early

- The 4% Rule Revisited: Safe Withdrawal Rates for Modern FI

How to keep the loop alive

If you want a simple way to stay in contact with the system between quarterly reviews, the 1% Better app is built for that.

It is not about optimization theater.

It is a consistency layer: small recurring check-ins that help you notice drift earlier, protect what matters, and stay connected to the systems you are trying to improve.

That is how FI starts behaving less like a distant number and more like a system you can trust.