Part 2: Sequential vs. Blended vs. Cyclical: Which Drawdown Strategy Fits?

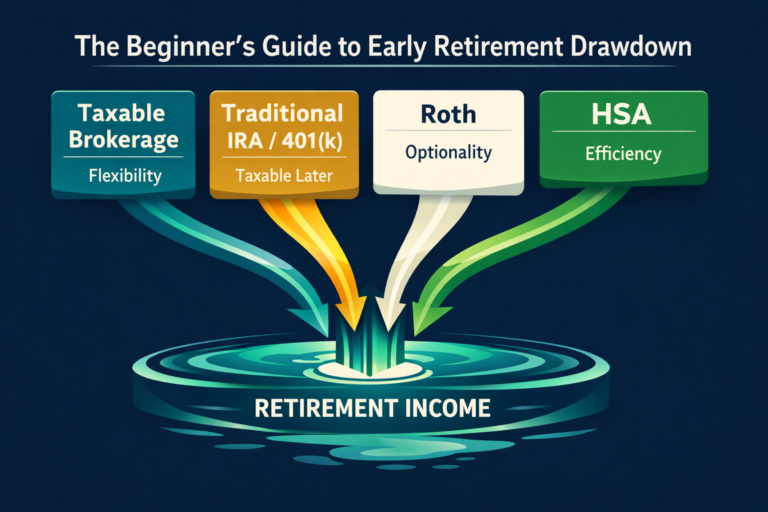

Part 1 covered the beginner view of early retirement drawdown: what the account buckets are, why the order matters, and why sequence-of-returns risk can make retirement harder than accumulation.

Part 1 taught you the buckets. Part 2 teaches you how to use them without creating unnecessary taxes or fragility.

This article is the next layer.

Once you understand the basic buckets, the real question is not simply which account comes first? The real question is: Which withdrawal strategy gives you the best combination of flexibility, tax efficiency, and long-term sustainability?

That is where sequential, blended, and cyclical drawdown come in.

Part 1 gave you the buckets. This article is about choosing how to use them without creating avoidable tax drag.

The buckets tell you what you have. The strategy tells you how to use them. And the wrong strategy can quietly increase taxes, reduce flexibility, or create future RMD problems. That is why choosing the right drawdown approach matters.

This article introduces Roth conversions, RMD pressure, and healthcare only as strategy inputs. Part 3 owns the deeper mechanics.

Why this question matters

At first glance, drawdown seems like a simple sequencing problem.

- Spend taxable money first.

- Then tap tax-deferred accounts.

- Then use Roth assets.

- Avoid making things more complicated than they need to be.

That is a useful beginner rule.

But once your retirement spans decades, the answer gets more complicated. The strategy you choose changes:

- how much tax you pay each year

- how much flexibility you keep for later

- how fast you consume traditional retirement accounts

- how much future RMD pressure you create

- how much room you have for Roth conversions

- how much room you preserve for healthcare planning

So this is not just a mechanics question. It is a tax-and-flexibility question.

The three main drawdown approaches

| Strategy | Best for | Strength | Watch-out | Not ideal for |

|---|---|---|---|---|

| Sequential | Simplicity-seekers | Easy to understand and execute | Can create future tax spikes | Large pre-tax balances |

| Blended | Tax-aware planners | Smooths income and improves bracket control | Requires monitoring | People who want autopilot |

| Cyclical / dynamic | Active planners | Most adaptable to markets, income, and tax changes | More complex; not automatically safer | Beginners or low-flexibility budgets |

The point of the table is simple: the best strategy is the one that fits your account mix, tax exposure, and willingness to manage the plan each year.

1. Sequential drawdown

Sequential drawdown means using one bucket before moving to the next.

The most common version is:

- Taxable accounts first

- Traditional accounts next

- Roth accounts last

This is the cleanest approach conceptually. It is easy to explain and easy to execute. Sequential works best when taxable accounts are large enough to fund many years without letting too much growth compound untouched inside pre-tax accounts.

Why people like it

- It is simple.

- It preserves tax-advantaged growth longer.

- It gives the retiree a clear order of operations.

Where it can break down

Sequential drawdown can leave too much money in pre-tax accounts for too long.

That can create:

- larger future RMDs

- higher taxable income later

- less room for low-bracket Roth conversions

- more risk of being forced into ugly tax years later in retirement

In other words, sequential can be neat, but not always efficient.

2. Blended drawdown

Blended drawdown means using multiple buckets in the same year.

Instead of fully emptying one account before touching another, you may:

- spend some taxable money

- take some traditional income up to a target bracket

- leave some Roth untouched for flexibility

For example, a retiree might take $20,000 from taxable, $15,000 from a traditional account up to a target bracket, and leave Roth untouched for later flexibility.

This is often the more tax-aware approach.

Why people like it

- It can smooth taxable income over time.

- It can help fill lower tax brackets intentionally.

- It can reduce future RMD pressure.

- It can create more balanced long-run outcomes.

Why it matters

A blended approach recognizes that the goal is not to win on one year’s tax return. The goal is to optimize across retirement as a whole.

That means you may deliberately take some income earlier if it reduces a future tax spike later.

3. Cyclical or dynamic drawdown

Cyclical drawdown means adjusting your withdrawal mix based on market conditions, income conditions, and tax conditions. Dynamic means the withdrawal mix changes based on markets, taxes, and income — not on a fixed formula.

This is the most flexible approach.

It says:

- use more taxable money in one year if markets are down

- increase Roth use when bracket management matters

- use traditional withdrawals when low-income windows are available

- adapt rather than lock yourself into one fixed formula

Why people like it

- It responds to reality instead of rigid rules.

- It can help manage sequence-risk exposure when paired with real spending flexibility.

- It gives you more control in volatile years.

Why it is harder

- It requires more judgment.

- It requires better tax modeling.

- It is less intuitive for beginners.

Cyclical drawdown is usually not the first strategy a new retiree should try to understand. But it is often where the best long-run plans end up.

Important caveat: dynamic drawdown does not automatically solve sequence risk. It can help only when it is paired with spending flexibility, cash reserves, rebalancing discipline, tax-aware withdrawal choices, and a willingness to cut spending or change course if markets are weak.

Why tax brackets change the answer

The biggest reason sequential drawdown is not always optimal is tax brackets.

Tax brackets create opportunities. A smart drawdown plan fills low brackets intentionally, avoids pushing income into high brackets unnecessarily, and uses early low-income years to reduce future tax pressure.

That means the plan should ask:

- How much room do I have in my current bracket?

- Can I fill that space intentionally?

- Should I pull more from traditional accounts now so I avoid bigger problems later?

- Can I harvest gains at favorable rates?

This is where the simple model starts to evolve.

A retiree with a large taxable account and modest pre-tax balance may favor one path.

A retiree with a huge traditional IRA may favor another.

A retiree with meaningful Roth balances may have still more flexibility.

The correct strategy depends on the tax map.

Why ACA and RMDs matter

Two planning variables often get overlooked when people discuss drawdown:

1. ACA subsidy impact

If you are in early retirement and buying health insurance on the exchange, income can influence your premium subsidies.

That means an extra dollar of income may do more than increase taxes. It may also affect healthcare costs.

So when you decide whether to blend withdrawals or stay sequential, you are not just choosing a tax rate. You are choosing a whole income profile.

Income affects both taxes and healthcare. Pre-tax balances affect future control.

2. RMD pressure

If you leave too much in tax-deferred accounts, future required minimum distributions can become a major problem.

That is especially true if:

- you retire early

- you have a long time horizon

- you expect meaningful investment growth

- you want more control later in life

The earlier you start thinking about RMD pressure, the more tools you have.

That does not mean you should blindly drain pre-tax accounts too fast. It means the future tax burden needs to be part of the conversation.

3. Why this still is not the advanced mechanics article

At this stage, you only need the headline: income timing affects both taxes and healthcare, and future forced distributions can distort your later years.

Part 3 goes deeper into the conversion math, law caveats, and annual planning process.

Where Roth conversions fit

Roth conversions are one of the most important intermediate-level tools in retirement planning.

A conversion moves money from a traditional account into a Roth account. You pay tax now so future qualified withdrawals can be tax-free.

That sounds simple, but the timing matters.

Why low-income years matter

Early retirement often creates low-income windows:

- you may no longer have earned income

- you may not yet have Social Security

- you may have space in lower tax brackets

Those are often the years where Roth conversions are most attractive.

Why this matters for drawdown strategy

If you use a purely sequential approach and ignore conversions, you may delay an important planning opportunity.

A blended or cyclical strategy can:

- create room for conversions

- reduce future RMDs

- increase Roth flexibility later

- improve tax diversification

This is where the intermediate version of drawdown becomes meaningfully different from the beginner version.

A simple decision matrix

Use this as a quick filter before you get into detailed modeling.

Start with sequential if:

- you want a simple rule that is easy to remember

- your traditional balances are modest

- your priority is reducing complexity, not optimizing every bracket

Move toward blended if:

- you have meaningful traditional balances

- you want to manage brackets deliberately

- you care about future RMD pressure and tax smoothing

Consider cyclical if:

- you can adjust spending when markets are weak

- you track taxes and cash flow each year

- you are comfortable using rules that change with income, markets, and healthcare costs

A useful shortcut is this:

- Simple and stable? Start sequential.

- Tax pressure and RMDs matter? Blend withdrawals.

- You can actively manage the plan each year? Consider a cyclical framework.

The point is not that one strategy is universally best.

The point is that the right strategy depends on what problem you are solving.

The goal is not to find the perfect strategy. It is to avoid the wrong one for your situation.

A practical example

Imagine two early retirees with the same $2 million portfolio.

Retiree A

- mostly taxable assets

- modest traditional balance

- some Roth flexibility

- prefers simplicity

Sequential drawdown is probably reasonable here.

Retiree B

- large traditional IRA

- meaningful taxable account

- some Roth, but not enough to cover everything

- expects a long retirement horizon

A more blended approach may be better here because the future RMD risk is much more relevant.

Same portfolio size. Completely different tax exposure. Very different answer.

That is why drawdown is not just a math question. It is a structure question. This is why the strategy matters more than the sequence.

What this means in practice

If you are still in the early stage of retirement planning, do not start with advanced modeling.

Start with:

- account buckets

- withdrawal order

- tax bracket awareness

- healthcare impact

- future RMD pressure

Then build from there.

The best plans usually do not start with sophistication. They start with visibility.

What comes next

Part 3 will go deeper.

Part 3 is where the strategy becomes a system — conversions, RMD suppression, healthcare timing, and long-term tax design.

That is where we move from strategy comparison into advanced FI planning:

- Roth conversion break-even logic

- RMD suppression

- account location

- healthcare and IRMAA planning

- Social Security timing

- survivor and estate considerations

In other words: the full tax mechanics of retirement.

Take the next step

If this article made your account mix feel more important than a single withdrawal rule, that is the right takeaway. FI Architect for iOS can help you test FI assumptions, compare scenarios, and see how changes in spending, taxes, inflation, debt, and investment assumptions affect the bigger plan.

Use the tool for visibility, not certainty. The goal is to make better decisions with a clearer model.

- Explore FI Architect for iOS

- Continue to Part 3: Advanced FI Planning

- Back to Part 1: The Beginner’s Guide to Early Retirement Drawdown

Sources and further reading

- BiggerPockets Money Podcast — The Ultimate Guide to Early Retirement Drawdown (2026)

- BiggerPockets Money Podcast — The Case for Blended (Instead of Sequential) Drawdown for Early Retirees

- BiggerPockets Money Podcast — The Four Fundamentals of Retirement Drawdown

- ChooseFI — Safe Withdrawal Rates, Drawdown Strategies, RMDs and 50 Year FI Timelines

- Fidelity — Savvy tax withdrawals

- T. Rowe Price — Tax-efficient retirement withdrawal strategies

- Journal of Accountancy — Tax-efficient drawdown strategies in retirement

- Charles Schwab — What Is Sequence-of-Returns Risk?

Disclosure

This article references concepts discussed on BiggerPockets Money, ChooseFI, Fidelity, T. Rowe Price, and other public retirement-planning sources. NJL Design Lab is not affiliated with, endorsed by, or sponsored by those publications or their creators. Any podcast or brand names are used solely for nominative fair use purposes to identify the source of the ideas being discussed.