What’s Actually Inside Your Index Fund? Why the Mix Matters More Than the Label

On this page

Investing

Most investors use the phrase index fund as if it settles the question.

It doesn’t.

An index fund is a container — not a complete investing strategy. The real question is what that index contains, how it behaves inside the rest of your portfolio, and whether you can keep holding it when markets get uncomfortable.

That distinction matters more than most people realize.

A fund label can make a portfolio sound simple. But simplicity is only useful if it still works when the market drops, when concentration shows up, or when you realize the fund you picked isn’t as diversified as you assumed.

The label is not the strategy

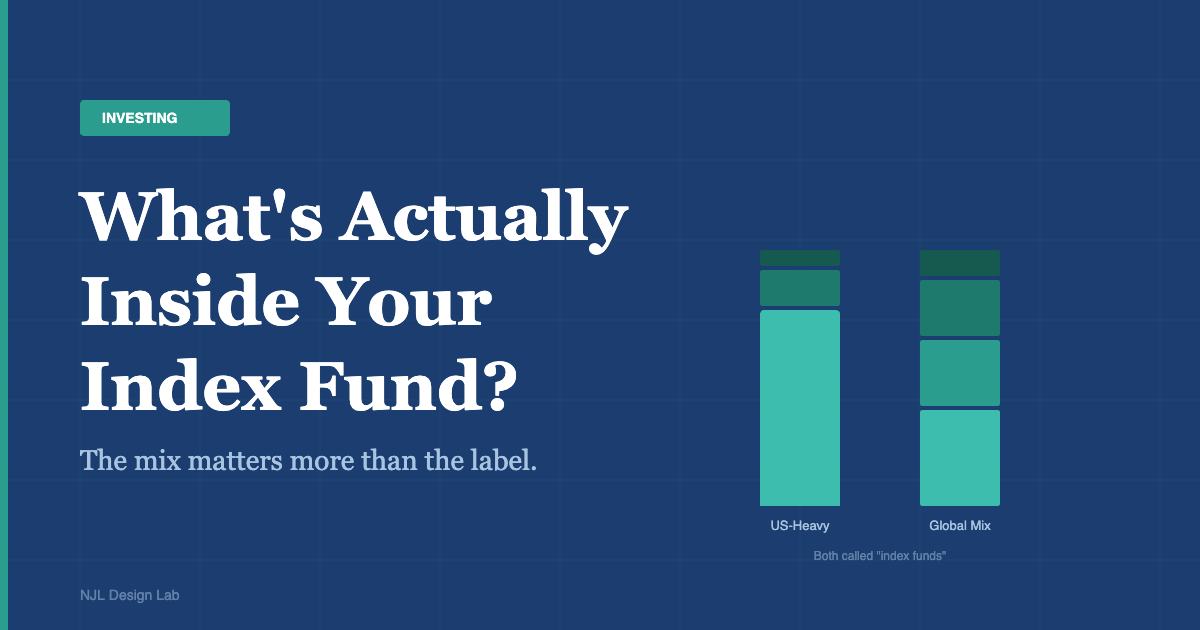

Two investors can both say they own index funds and still have very different portfolios.

One may own a broad U.S. market fund with heavy exposure to mega-cap technology companies. Another may own a global fund with meaningful international exposure and a different balance of sectors, regions, and currencies. Both can be called index investors. Both can be low-cost. Both can be passive.

They are still not the same portfolio.

That is why the label matters less than the mix.

The fund tells you how the money is managed. The mix tells you what risk you are actually taking.

What an index fund actually gives you

At a basic level, an index fund follows a rule set. It does not try to outguess the market — it tracks a defined basket of assets. In practice, that means the design of the index matters just as much as the fund wrapper itself.

A market-cap weighted index fund will naturally give more weight to larger companies. That is not a flaw. It is the design. But it does mean the fund may be more concentrated than many investors realize.

A low fee does not automatically make a fund well diversified. It only means the fund is cheap to own. Those are related but different ideas.

If you want to understand what you own, look past the fund name and ask:

- What is inside the index?

- How is it weighted?

- What regions does it emphasize?

- What does it leave out?

- How does it behave relative to the rest of my holdings?

That is the real work.

Why the mix matters more than the label

The biggest mistake is assuming one index fund automatically solves every portfolio problem.

It does not.

A portfolio is still a portfolio, even if every piece inside it is passive. That means the important decisions still exist:

- How much should be in stocks?

- How much should be in bonds?

- How much concentration are you willing to accept in one market, one country, or one sector?

- How much complexity are you willing to carry for the sake of a slight theoretical edge?

These are strategy questions, not product questions. The product can be excellent and still be the wrong fit.

If your allocation is too aggressive, you may panic in a downturn. If it is too conservative, you may not get the growth your plan needs. If it is too concentrated, you may think you are diversified when you are really just holding many versions of the same risk.

Diversification is about correlation, not variety

A lot of people use diversification to mean “having many things.” That is not enough.

Real diversification is about how assets behave relative to each other. If all of your holdings tend to fall together, you do not have much protection — you have variety, but not real diversification.

That is why stock and bond mix still matters. That is why home country bias matters. That is why international exposure matters. And that is why concentration risk can still exist inside a seemingly broad fund.

The key distinction: The point is not to make the portfolio complicated. The point is to make the risk honest. If you want stability, your holdings must actually behave differently under stress — not just carry different names.

If you want growth, the portfolio needs enough equity exposure to compound over time. If you want both stability and growth, you have to decide how those goals trade off against each other.

Simplicity works when it is intentional

There is a difference between simple and simplistic.

Simple means the portfolio is easy to understand, easy to maintain, and strong enough to hold through bad markets. Simplistic means it was oversimplified to the point that it no longer matches reality.

A good portfolio does not need to be clever. It needs to be coherent.

That usually means:

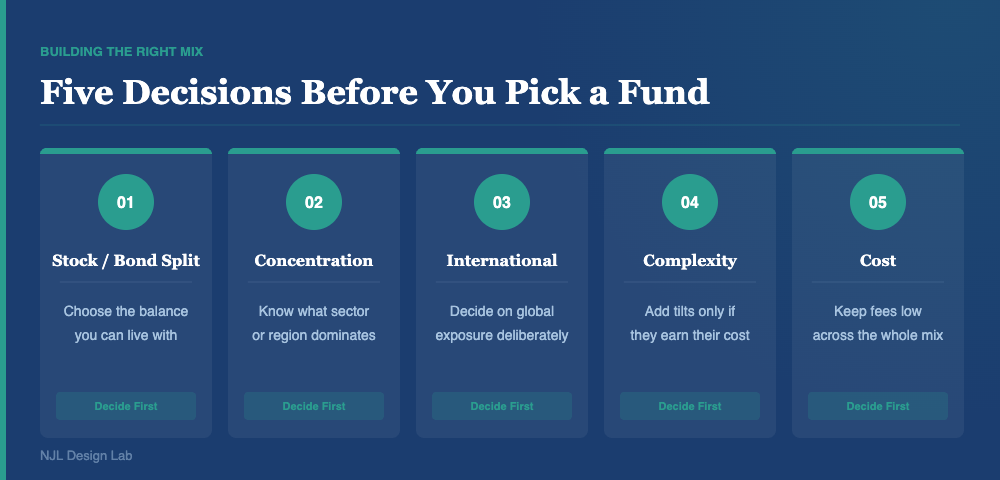

- Picking a stock/bond balance you can actually live with

- Understanding what kind of concentration you are accepting

- Keeping costs low enough that the portfolio earns its keep

- Avoiding complexity that does not clearly improve outcomes

- Being honest about how much volatility you can actually endure

If you add complexity, do it on purpose — not because it sounds sophisticated. The best portfolio is not the one with the most moving parts. It is the one you can still believe in after a bad year.

How to choose a better mix

Start with the purpose of the money.

If this is long-term retirement capital, the portfolio needs growth. If the money may be needed sooner, the portfolio needs more stability. If the goal is to stay invested without second-guessing every move, the portfolio needs to match your real tolerance for risk — not your optimistic self-image.

Then work from the top down:

- Decide the stock/bond balance.

- Decide how much concentration you are willing to tolerate.

- Decide whether international exposure belongs in the mix.

- Decide whether any tilts are worth their long-term complexity.

- Keep costs low enough that the portfolio earns its keep.

That is a more useful process than searching for the perfect fund. Because once the mix is right, the fund selection gets much easier.

The bottom line

An index fund is a tool. A portfolio is the system.

If you confuse the two, you may end up with something that sounds passive but behaves like a portfolio you never actually designed.

The better question is not “Which index fund should I buy?”

It is “What mix of assets do I actually want to hold through a full market cycle?”

Answer that honestly, and the rest becomes a lot clearer.

Take the next step

Once your portfolio mix is clear, the next question is what it needs to sustain you in retirement. These tools and reads will help: