The Boring Middle of Financial Independence Isn’t Boring. It’s Identity Work.

On this page

- The middle of FI feels slower for a reason

- FI is no longer just about getting there

- Why net worth stops feeling emotionally sufficient

- The real shift: accumulator to maintainer

- The middle carries a different kind of stress

- What changes in the middle

- How to stay grounded in the boring middle

- Boring is evidence of stability

- Next Steps

- If you want to reduce how much you need

- If you want to understand what happens after accumulation ends

- If you want the milestone that defines the end of the hard part

- The boring middle is easier when you can see it clearly.

The middle of FI feels slower for a reason

The middle of financial independence is where many people expect the journey to feel easier.

In theory, the hardest part should be over. The account balances are larger. The savings habit is already built. The system is working. But emotionally, the middle often feels flatter than the beginning. Progress is still happening, just not in a way that feels dramatic.

That is why people call it the boring middle.

But boring is the wrong frame.

What looks boring is usually the point where FI stops being a math problem and starts becoming an identity problem. Early FI is about accumulation. The middle is about durability. And that shift changes everything.

“Boring is not failure. Boring is evidence that the system works.”

“The middle is where financial independence becomes a life, not just a target.”

FI is no longer just about getting there

At the start of the journey, the goal is clear: save more, invest more, build momentum, and move toward independence.

That phase has urgency. Every milestone is visible. Every percentage point matters. Every good decision feels like acceleration.

The middle is different.

You are no longer only asking, “How do I get there?” You are also asking, “Who am I becoming while I get there?”

That second question is what makes the middle feel more complicated. The math still works, but the story becomes less dramatic. There is less novelty. Less urgency. Less obvious proof that the system is paying off.

That does not mean the system is broken.

It means the work has changed.

Why net worth stops feeling emotionally sufficient

A larger portfolio does not always feel like enough.

That is not a flaw in the plan. It is a feature of human psychology.

As your net worth grows, the line between “almost there” and “actually enough” can feel frustratingly fuzzy. The number is higher, but the feeling is not always proportional. You may have more options than ever and still feel uncertain about whether you are on track.

That is one reason the middle can feel emotionally expensive.

If your self-image is still built around “I am trying to reach FI,” then every delay feels like friction. If your self-image has shifted toward “I am already living with more intentionality,” then the middle becomes easier to inhabit.

The number matters. But the number is not the whole experience.

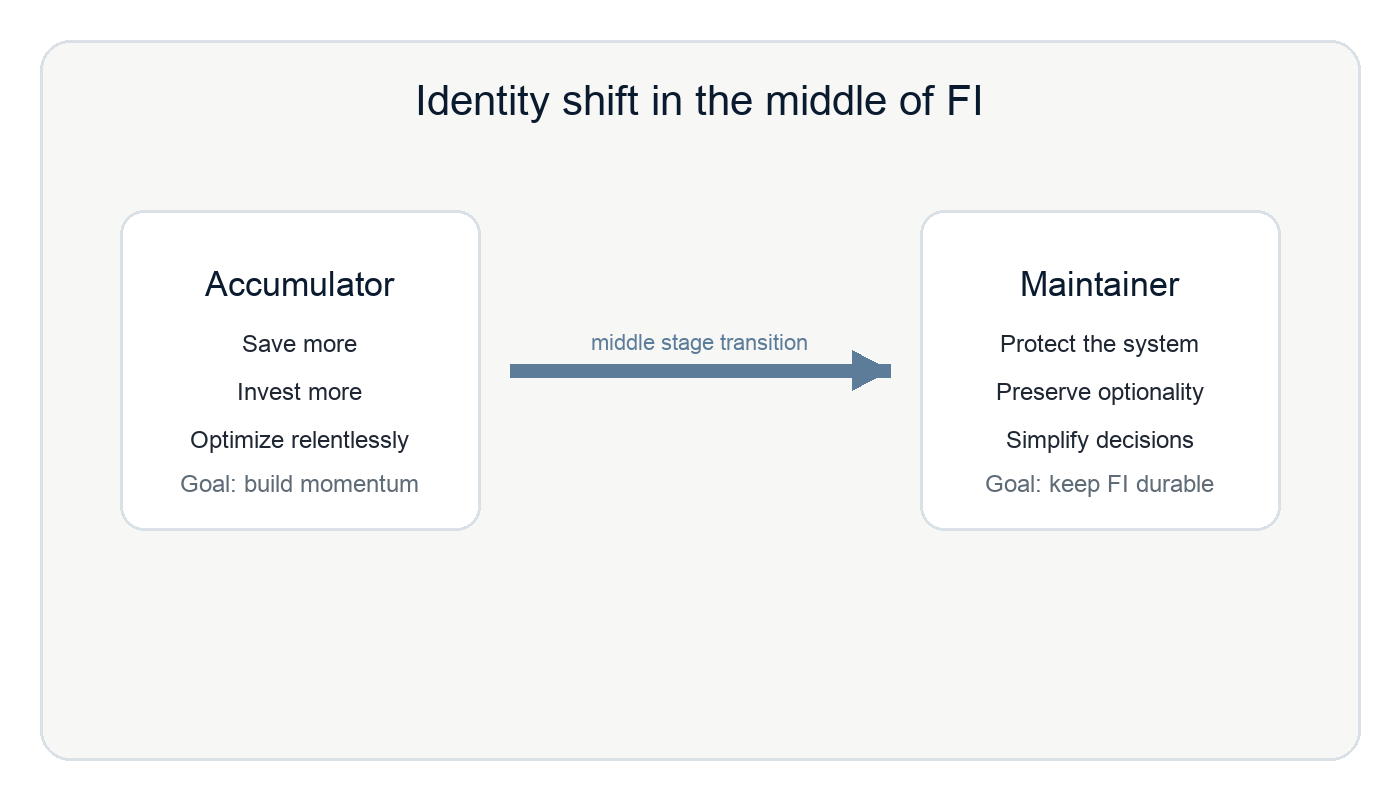

The real shift: accumulator to maintainer

The boring middle often marks a change in role.

At first, you are an accumulator. You optimize. You save. You push. You build.

Later, you become a maintainer. You protect the system. You preserve optionality. You make decisions that keep the plan durable.

That shift sounds subtle, but it changes how you think about almost everything:

- spending

- work

- time

- risk

- family

- energy

You stop asking only how to maximize. You start asking what is worth preserving.

That is a more mature FI posture.

And it is one of the healthiest signs that the plan is working.

The middle carries a different kind of stress

The middle of FI is not stressful because nothing is happening. It is stressful because too much is changing quietly.

Common middle-stage feelings include:

- impatience

- comparison

- fear that progress is too slow

- worry that the current life is passing by

- uncertainty about whether FI will actually feel different when it arrives

Those feelings are normal.

They do not mean you are ungrateful. They mean you are aware of the tradeoffs.

The middle is where many people confront the real question: what is FI for?

If the answer is only “to stop working,” the middle can feel hollow. If the answer includes flexibility, calm, family time, and a more deliberate life, the middle has more meaning.

That is why this phase matters so much. It forces clarity.

What changes in the middle

The middle is where FI starts affecting daily life before the full exit happens.

You may notice that:

- spending becomes more values-based

- work becomes more optional

- decisions get less reactive

- the future feels less fragile

- you stop needing every choice to be an optimization contest

That is real progress.

FI is not only a destination. It is a way of improving the quality of your current life while still on the path.

This is also where simple systems matter most. The people who stay grounded in the middle are rarely the people chasing excitement. They are usually the people who built something sustainable:

- simple spending

- low-friction routines

- clear financial tracking

- honest annual check-ins

- fewer unnecessary commitments

The middle rewards consistency more than intensity.

How to stay grounded in the boring middle

If the middle feels slow, do not ask only whether you are progressing fast enough. Ask whether your system is still aligned.

A useful checklist:

- Are you measuring only net worth, or also optionality?

- Are you protecting the parts of life that already feel good?

- Are you making the middle livable now, not just later?

- Are you letting comparison distort your sense of progress?

- Are you building a life that can carry FI when it arrives?

That last question matters most.

FI should not only produce freedom later. It should also improve the quality of your current life.

When the middle is working well, it does not feel flashy. It feels calm, deliberate, and durable.

Boring is evidence of stability

The boring middle is not a waste of time.

It is the phase where financial independence becomes something more than a target. It becomes a way of living.

That usually looks less dramatic than people expect. But it is also more valuable than people expect.

Because once you stop treating the middle like a waiting room, you can see what it really is:

- a season of increased optionality

- a test of identity

- a chance to simplify before the finish line

- the place where financial independence becomes real before it becomes complete

In that sense, boring is not failure. Boring is evidence that the system works.

Next Steps

The boring middle is easier to navigate when you know exactly where you stand. Three articles worth reading from here, depending on what you are working through:

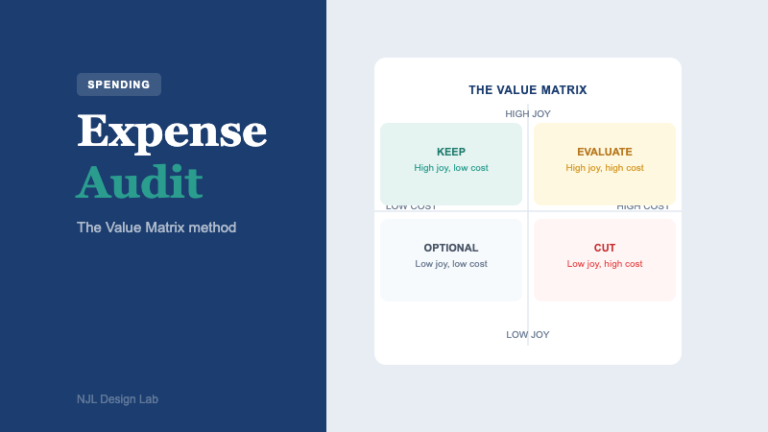

If you want to reduce how much you need

Most people in the FI middle are carrying discretionary spending they have never audited. The Value Matrix is a practical framework for separating spending that genuinely serves your life from spending that just shows up on the statement.

If you want to understand what happens after accumulation ends

The middle eventually ends. When it does, the question shifts from “how much do I need?” to “how do I draw this down without running out?” The 4% rule is where most people start — and where most people stop reading too soon.

If you want the milestone that defines the end of the hard part

CoastFI is the point where your invested assets are already large enough to reach your retirement number on their own — without another dollar of contributions. For many people in the boring middle, CoastFI is closer than they think.

Keep the numbers honest

The boring middle is easier when you can see it clearly.

FI Architect is the free planning tool built for exactly this phase — model your FI number, track your timeline, and run scenarios that show how different assumptions change when you cross the line. No spreadsheet setup required.