Options Trading 101: What Beginners Need to Know Before Selling a Put

On this page

- A simple mental model

- Before you start trading

- What an options contract actually is

- Key terms to keep straight

- Calls vs. puts

- Why selling a put creates an obligation

- Cash-secured puts: the beginner strategy that still requires discipline

- Assignment: what happens when the put is exercised

- Where the wheel strategy fits

- Covered calls: the next contract after share ownership

- What you are agreeing to

- A simple covered call example

- When covered calls can make sense

- The dividend and early-assignment wrinkle

- The covered call checklist

- Common beginner mistakes

- Approval, suitability, and why beginners should slow down

- What to remember

- Quick checklist before you trade

- FAQ

- Is selling puts safe for beginners?

- What happens if my put is assigned?

- Is the wheel strategy good for passive income?

- What is the difference between a cash-secured put and a naked put?

- Sources and further reading

- Build the decision system around the trade

Most beginners learn options backward.

They jump into strategies before they understand the contract underneath them — and that is where the confusion begins.

That is why options feel more confusing than they need to. The mechanics are direct, but the strategy comes too early for most new readers.

If you are looking at options for the first time, the goal should not be to memorize every strategy. The goal should be to understand the mechanics well enough to recognize risk, read the setup correctly, and avoid treating a trade like a shortcut.

This guide focuses on the pieces beginners usually need before selling a put: calls, puts, assignment, cash-secured puts, the wheel strategy, and the covered call step that can come after share ownership.

A simple mental model

Keep this rule in mind:

- The buyer gets a right.

- The seller takes on an obligation.

That is the core tradeoff. If you remember nothing else, remember that the person selling the option is taking the other side of a contract, not buying a lottery ticket.

Before you start trading

Do not start with premium. Start with the contract.

- What right is being created?

- What obligation are you accepting?

- What happens if assignment occurs?

- Can you afford that outcome without disrupting the rest of your plan?

What an options contract actually is

An option is a contract tied to a stock, ETF, or another underlying asset. It has a strike price, an expiration date, and a premium. Those three pieces define what the contract can do, how long it can do it, and what the buyer pays the seller for taking the other side.

At the highest level, options are built around a simple question: Who has the right, and who has the obligation?

That question matters because the buyer and the seller do not occupy the same position.

The buyer pays premium for choice. The seller receives premium for taking on a possible obligation.

Key terms to keep straight

- Strike price: the price where the contract can be exercised.

- Expiration: the date when the contract ends.

- Premium: the price paid by the buyer and received by the seller.

- Assignment: the moment the seller’s obligation becomes real.

- In the money / out of the money: whether the contract currently has exercise value based on the stock price and strike.

Calls vs. puts

There are two basic kinds of options: calls and puts.

A call gives the holder the right to buy the underlying asset at a set price. A put gives the holder the right to sell it at a set price. For standard U.S. equity options, that right can generally be exercised before expiration, though many contracts simply expire or are closed before assignment ever happens.

Keep the key distinction simple:

- Buying an option means paying for the right.

- Selling an option means taking on the obligation if the contract is exercised or assigned.

For beginners, that second part is the one to slow down on.

Why selling a put creates an obligation

When you sell a put, you are not just “placing a trade.” You are taking responsibility for a possible outcome.

If the put is assigned, you may be required to buy the underlying shares at the strike price. That is why cash-secured puts are called cash-secured. The strategy assumes you are setting aside enough cash to satisfy that obligation if assignment happens.

This is the first place where options stop being abstract and start becoming concrete.

A simple example helps.

Imagine a stock trading at $50.

You sell a put with a $45 strike price.

You collect a premium for taking the other side of that contract.

If the stock stays above $45, the put may expire worthless and you keep the premium.

If the stock falls below $45, assignment becomes a live possibility and you may be required to buy shares at the strike price.

That is not a bonus feature. It is the structure of the trade.

Cash-secured puts: the beginner strategy that still requires discipline

A cash-secured put is a way of selling a put while reserving enough cash to buy the shares if assignment occurs.

That framing matters because it removes the fantasy. You are not getting free income. You are taking a defined risk in exchange for premium.

In the right situation, that can be a sensible way to express a view on a stock or ETF you already want to own at a lower price. But it only works if you are honest about the tradeoff:

- You collect premium up front.

- You give up the chance to participate in upside beyond that premium unless you already own the shares separately.

- You take on downside if the stock falls sharply.

- You may end up owning the shares sooner than expected.

The strategy is simple to describe and more serious to manage.

Before selling a put, the cleaner question is not “How much premium can I collect?” It is “Would I be comfortable owning this position at this effective price if assignment happens?”

Assignment: what happens when the put is exercised

Assignment is the moment the contract gets completed.

For a put seller, that means the obligation becomes real. If the contract is assigned, you buy the shares at the strike price.

Assignment usually becomes more likely when the option is in the money near expiration, but it is not limited to the final day. The exact mechanics depend on the option, the broker, and the holder’s decision to exercise.

Imagine this sequence:

- You sell a put with a $45 strike.

- The stock drops to $43.

- The option is assigned.

- You now buy the shares at $45.

That is why beginners sometimes fear assignment: it feels like the trade moved against them. But assignment is not a hidden surprise. It is the contract finishing the way the contract was written.

If you sell puts, you need to be comfortable with the possibility that the trade can end in share ownership. That is especially important when the market moves quickly or when the stock price finishes below the strike.

The key lesson is not to fear assignment. Assignment is not inherently bad if it fits the plan you already built. The problem is being surprised by it after the trade is already live.

If assignment would make you panic, the trade is too large, the stock is the wrong fit, or the strategy is the wrong fit.

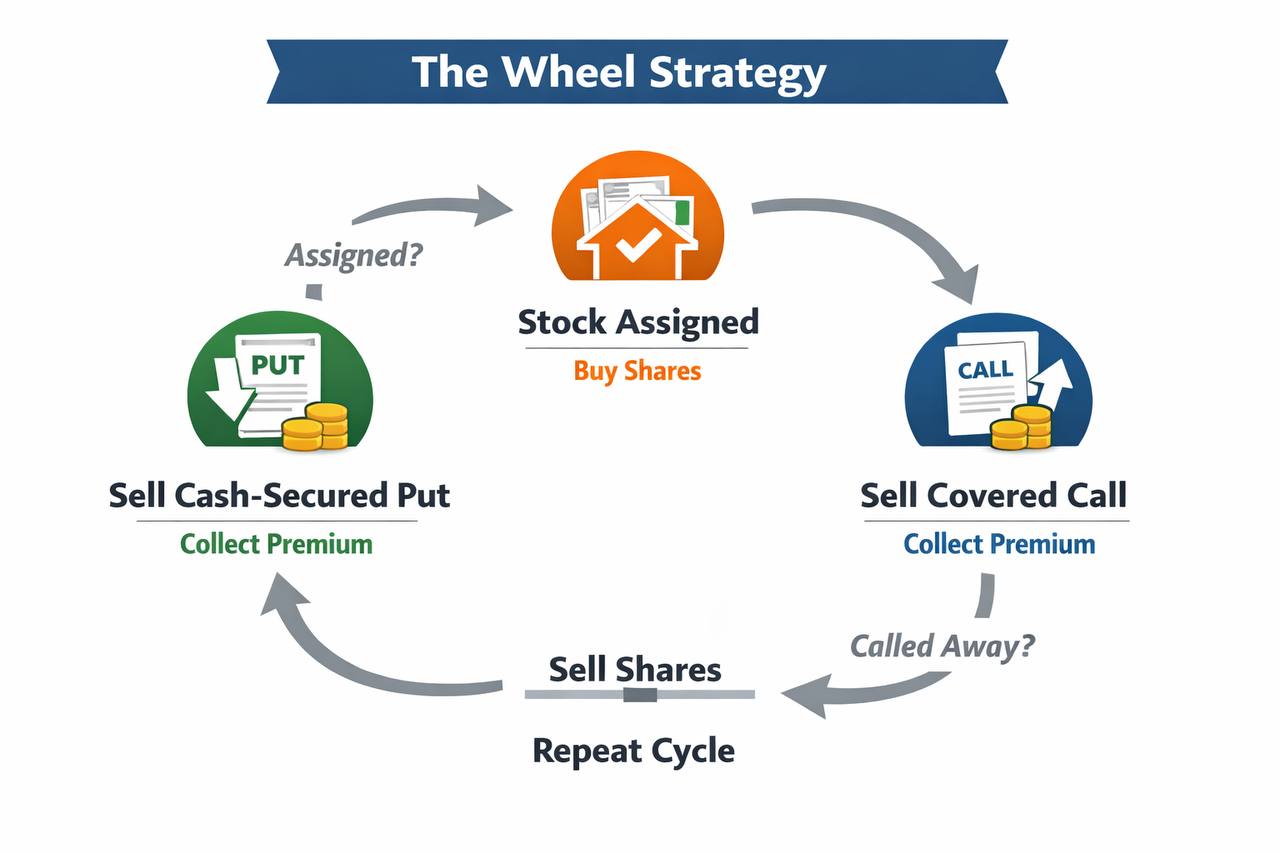

Where the wheel strategy fits

The wheel strategy is often discussed as a sequence:

- Sell a cash-secured put.

- If assigned, own the shares.

- Then potentially sell covered calls against those shares.

That can be a useful framework for understanding how options strategies connect. But it should not be treated like a promise.

The wheel only works if you treat each step as a contract with obligations, not as a passive income machine.

What the wheel is good for:

- showing how a put sale can lead into share ownership

- giving a repeatable structure to traders who understand assignment

- connecting one options decision to the next in a disciplined way

What the wheel is not good for:

- passive income claims

- shortcut thinking

- assuming neat outcomes or guaranteed premium collection

- ignoring concentration risk in a stock you only partly wanted to own

The wheel is a structure for working through a repeatable process with clear obligations and clear tradeoffs.

That makes it worth learning.

It does not make it risk-free.

Covered calls: the next contract after share ownership

A covered call is an options trade where you already own at least 100 shares of the underlying stock or ETF and then sell a call against that position.

It is called “covered” because your shares cover the obligation if the option is exercised. If the call is assigned, you deliver the shares you already own. That is very different from selling a naked call, where the potential loss can be much larger and much harder to control.

For many beginners, covered calls feel more approachable because the starting point is a stock position they already understand. But “more approachable” does not mean “free income.” A covered call changes the risk profile of a stock position. It does not remove the risk of owning the stock.

What you are agreeing to

When you sell a covered call, you collect premium and agree to sell your shares at the strike price if assignment happens.

That creates three possible outcomes:

- The stock stays below the strike. The call may expire worthless, you keep the premium, and you still own the shares.

- The stock rises above the strike. The shares may be called away, meaning you sell them at the strike price even if the market price is higher.

- The stock falls. The premium may soften the decline, but you still carry the normal downside risk of owning the shares.

That last point is essential. A covered call is not downside protection in any strong sense. It is a small buffer, not a shield. If the stock drops hard, the premium may reduce the pain slightly, but it will not prevent a large drawdown.

A simple covered call example

Imagine you own 100 shares at $50 per share.

You sell a covered call with a $55 strike and collect $1 per share in premium.

- If the stock stays below $55, the call may expire worthless and you keep the premium.

- If the stock rises to $60 and the call is assigned, you may still sell the shares at $55, not $60.

- If the stock falls to $42, the $1 premium helps a little, but you still own a position that has declined meaningfully.

The tradeoff is clear: you receive premium today, but you cap some of your upside tomorrow.

When covered calls can make sense

Covered calls tend to fit best when you already own the shares, understand why you own them, and would be emotionally and financially comfortable selling them at the strike price.

They can be useful when:

- you are willing to trim or exit the position at a specific price

- you want to generate premium from a position you already hold

- you are not relying on the stock for unlimited upside

- you understand that assignment is an acceptable outcome, not a failure

They are a poor fit when:

- you would be upset if the shares were called away

- the position is highly volatile and you do not understand the risk

- you are using premium to justify holding a stock you no longer believe in

- you are ignoring tax consequences, dividends, or concentration risk

The dividend and early-assignment wrinkle

Covered calls can also create early-assignment risk, especially around ex-dividend dates when the option is in the money. That does not mean every covered call will be assigned early. It means beginners should know that assignment can happen before expiration and should not build a plan that only works if the contract waits until the final day.

The practical question is simple: if your shares were called away tomorrow, would the outcome still fit your plan?

The covered call checklist

Before selling a covered call, walk through this checklist:

- Do I own at least 100 shares for each call contract?

- Am I comfortable selling those shares at the strike price?

- Do I understand how much upside I am giving up?

- Do I still want to own the stock if it falls?

- Have I checked dividend timing, tax consequences, and broker rules?

- Is the premium worth the obligation I am taking on?

A covered call can be a disciplined tool. It can also become a way to rationalize a weak position. The difference is whether the strike, timing, and assignment outcome fit your actual plan.

Common beginner mistakes

Most beginner options mistakes come from treating the strategy as easier than the contract underneath it.

- Selling puts on stocks you do not actually want to own. If assignment would leave you holding a position you dislike, the premium was not worth it.

- Underestimating assignment risk. Assignment is not a weird edge case. It is one of the normal ways a short option can resolve.

- Selling covered calls on shares you are emotionally attached to. If you would be frustrated selling at the strike, the covered call may not fit.

- Confusing premium with protection. Premium can soften a move. It does not remove the downside of owning the stock.

- Ignoring concentration risk. The wheel can quietly push more capital into one position than your portfolio can comfortably handle.

Approval, suitability, and why beginners should slow down

Most brokers require options approval before you can trade them. That is not a formality. It is a signal that the broker expects some level of suitability review before giving access to the product.

Brokers do that because options create contingent obligations and assignment risk, which means the consequences can change quickly.

That should matter to the reader.

If a strategy sounds easy but still requires approval, collateral, and a clear understanding of assignment, then it should not be treated like a casual first trade.

For beginners, the right posture is:

- learn the contract mechanics first

- understand the obligation second

- define the downside before you think about the premium

- only then decide whether the strategy fits your goals

This article is educational, not personal financial advice. Options are not appropriate for every investor, and the right decision depends on your risk tolerance, portfolio, time horizon, broker rules, and tax situation.

What to remember

If you remember only one thing, remember this:

An option is not a bet in the abstract. It is a contract with a defined right on one side and a defined obligation on the other.

Once that clicks, calls, puts, assignment, and cash-secured puts become much easier to understand.

And once those pieces make sense, you can evaluate the wheel strategy with a clearer head instead of treating it like a shortcut to easy returns.

Quick checklist before you trade

- What is the right?

- What is the obligation?

- What happens if I am assigned?

- Can I afford assignment?

- What happens if the stock moves sharply against me?

- What upside am I giving up?

- Does this fit my plan?

FAQ

Is selling puts safe for beginners?

Selling puts can be simple to understand, but that does not make it automatically safe. The risk is that you may be assigned and required to buy shares at the strike price. Beginners should understand the obligation, have the cash available, and only consider the strategy on positions they would be comfortable owning.

What happens if my put is assigned?

If your short put is assigned, you buy the shares at the strike price. That can be acceptable if you planned for it. It can be a problem if the position is too large, the stock has fallen sharply, or you never wanted to own the shares in the first place.

Is the wheel strategy good for passive income?

The wheel is better understood as a repeatable contract sequence, not passive income. It can collect premium, but it also creates assignment risk, stock ownership risk, capped upside during the covered call step, and concentration risk if too much capital ends up in one position.

What is the difference between a cash-secured put and a naked put?

A cash-secured put assumes you have enough cash set aside to buy the shares if assigned. A naked put does not have the same full cash reserve behind it and can introduce margin risk. For beginners, the cash-secured framing is cleaner because it forces the assignment outcome into the plan before the trade is placed.

Sources and further reading

This article uses official educational references for definitions, approval, assignment, and risk framing:

- Investor.gov: Investor Bulletin — An Introduction to Options

- Investor.gov: Opening an Options Account

- FINRA: Trading Options — Understanding Assignment

- OCC: Characteristics and Risks of Standardized Options

Build the decision system around the trade

Options are easier to evaluate when they are part of a broader financial system, not a standalone bet. If you want to keep building that framework, start with The Real Work in FI Is Not the Number. It’s the Control Loop.

You can also explore the broader NJL system here: