Part 1: The Beginner’s Guide to Early Retirement Drawdown

A simple model for account buckets, withdrawal order, and sequence risk.

If accumulation is the first half of financial independence, drawdown is the part most people underplan.

Drawdown feels harder because the stakes are higher — one wrong move can create taxes, penalties, or a lasting hit to portfolio longevity.

That makes sense. Building wealth feels concrete. You can automate contributions, increase income, improve savings rate, and watch the numbers rise. Drawdown is different. The questions get harder: Which account do you use first? How much can you spend without creating a future tax problem? What happens if the market drops early in retirement? And how do you turn a portfolio into income without turning the whole thing into a puzzle?

This guide is the beginner version. It is not the most optimized version. It is the version that helps you build the right mental model before you start making detailed tax decisions.

Beginner rule: simple first, optimized later.

If your account mix is complex, do not start by trying to optimize everything at once. Start with a clean withdrawal order, then improve the tax details later.

What drawdown actually means

Drawdown is the process of converting your accumulated assets into spendable retirement income.

That sounds obvious, but the distinction matters.

A portfolio is not the same thing as income. You can have a large net worth and still be poorly prepared if you do not know how to turn that balance into a sustainable spending plan. In retirement, the goal is not to “run the account down.” The goal is to fund life without forcing unnecessary taxes, penalties, or bad timing decisions.

That is why drawdown is a system, not a guess.

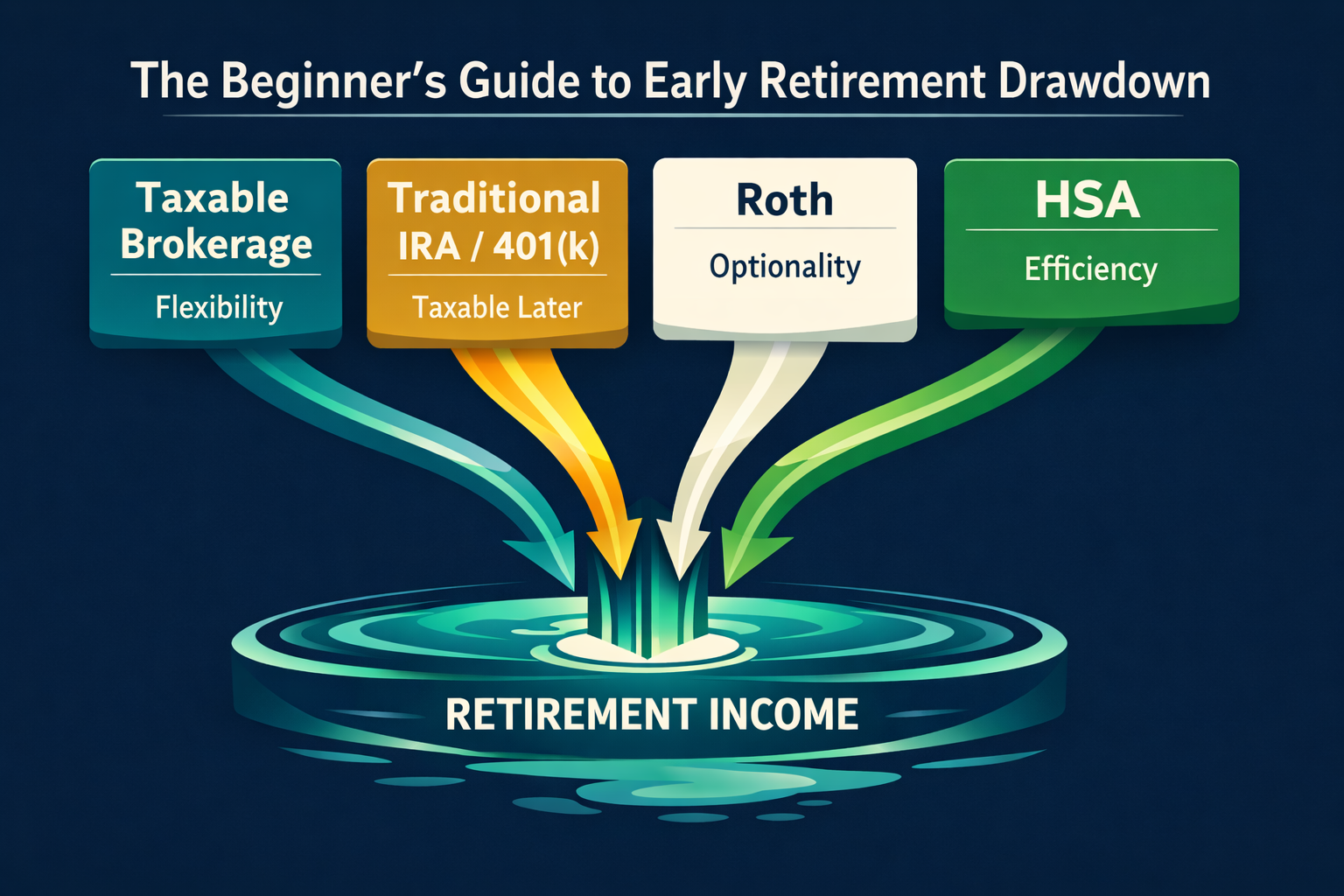

The four account buckets

Most early retirees are not drawing from one account. They are drawing from a mix of account types with different tax treatment.

1. Taxable brokerage

This is usually the most flexible bucket.

- You already paid tax on the principal.

- You may owe tax on gains when you sell.

- You can usually access the money without age-based restrictions.

For many people, this is the easiest place to start because it is the least structurally constrained.

2. Traditional 401(k) / IRA

This is the tax-deferred bucket.

- Contributions were generally pre-tax.

- Withdrawals are usually taxed as ordinary income.

- This bucket can become a future tax problem if it grows too large relative to everything else.

It is valuable, but it needs a plan.

3. Roth accounts

This is the tax-free bucket.

- Contributions were made with after-tax money.

- Qualified withdrawals are generally tax-free.

- Roth accounts are powerful because they create flexibility later.

Think of Roth as your most valuable optionality bucket.

4. HSA

If you have one, the HSA can be the most tax-efficient account of all.

- Contributions may be pre-tax or deductible.

- Growth can be tax-free.

- Qualified medical withdrawals can be tax-free.

For many people, the HSA is not a primary spending bucket in the early years, but it deserves to be part of the system.

If you want a simple picture: taxable is flexibility, traditional is taxable later, Roth is optionality, and HSA is efficiency.

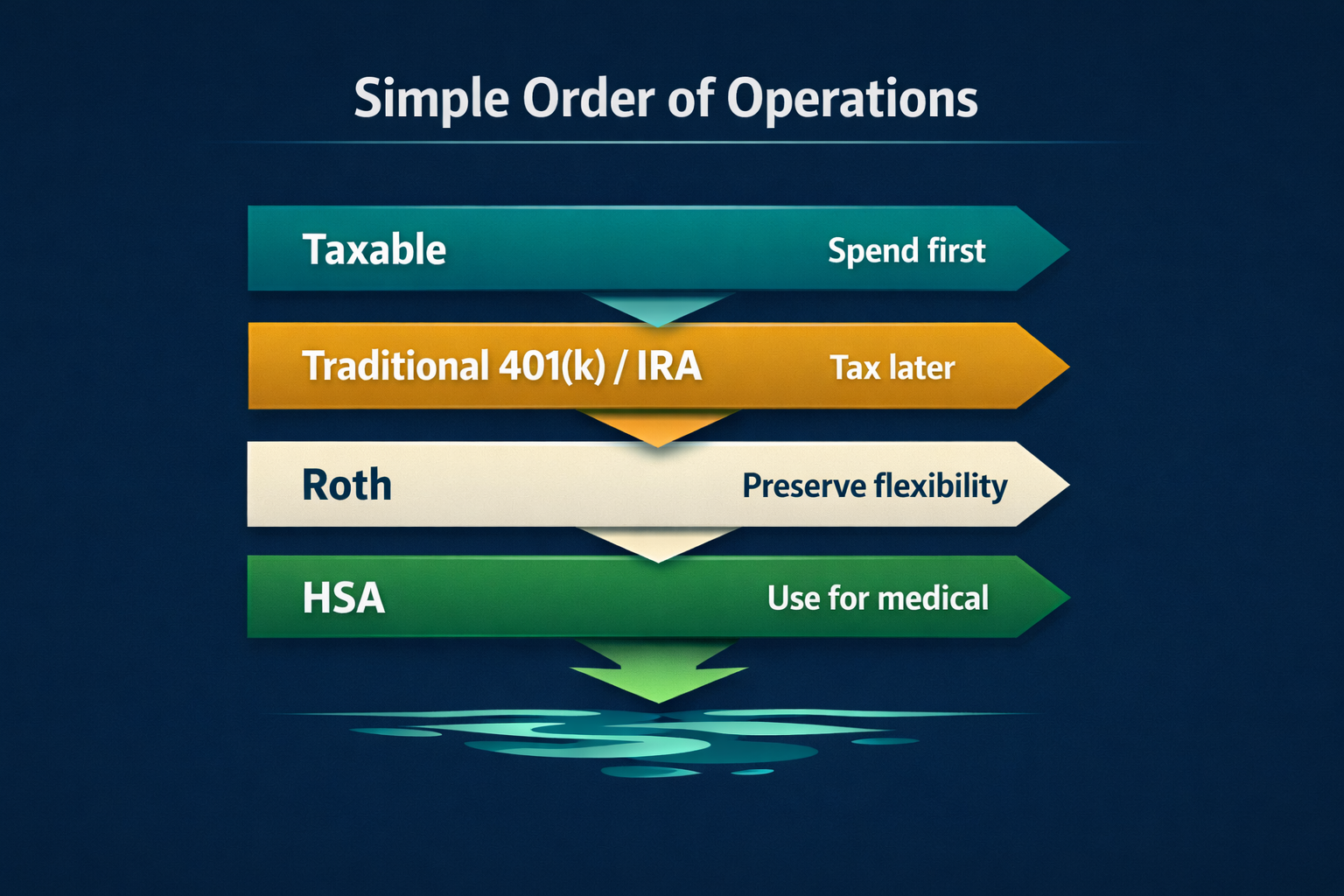

The simple order-of-operations model

Beginners usually need a starting point, not a perfect model.

A common rule of thumb is:

- Spend from taxable accounts first.

- Then use tax-deferred accounts.

- Then use Roth assets.

- Keep the HSA available for qualified medical expenses when relevant.

This order is popular because it is easy to follow and it preserves tax-advantaged growth for as long as possible.

It works as a beginner model because it spends the least constrained dollars first and preserves the most tax-advantaged dollars for later.

But the key word is starting point.

This order works reasonably well as a beginner frame, but it is not automatically optimal for every household. Later in the series, we will look at why blending withdrawals can sometimes reduce lifetime taxes and why aggressive early planning can reduce future RMD pressure.

Why sequence-of-returns risk matters

Drawdown is more fragile than accumulation because bad returns early in retirement can do lasting damage.

Here is the simple version:

- In accumulation, a bad market year can be annoying.

- In retirement, a bad market year can force you to sell more assets to fund the same spending.

- Selling more assets during a downturn leaves fewer assets to recover when the market rebounds.

That is sequence-of-returns risk.

Sequence risk is not about average returns. It is about the timing of withdrawals colliding with bad markets.

The order of returns matters because withdrawals interact with market performance. Two people can earn the same average return over time and still end up with very different outcomes depending on when the bad years happen.

This is why retirement planning is not just about average returns. It is about timing, cash flow, and flexibility.

Callout: Flexibility is a retirement asset.

The more room you have to adjust spending, taxes, and account choice, the less fragile your plan becomes.

A simple example

Imagine a retiree with:

- $1,500,000 in investable assets

- a mix of taxable, traditional, and Roth accounts

- a target annual spending level of $60,000

Suppose the first year looks like this:

- Start with $35,000 from taxable brokerage because it is the most flexible bucket.

- Add $15,000 from a traditional account to use some available low-bracket income space.

- Cover the remaining $10,000 from cash reserves, dividends, or another flexible taxable source.

- Keep Roth untouched for flexibility and future optionality.

- Hold back the HSA unless qualified medical costs show up.

Now the retiree can see the whole year in plain language:

- spending target: $60,000

- taxable brokerage / flexible taxable sources: $45,000

- traditional withdrawals: $15,000

- Roth withdrawals: $0

- HSA withdrawals: only if needed for medical expenses

In this example, the $15,000 traditional withdrawal might fill part of the 10% or 12% federal bracket, depending on the household. That is the point: the retiree is not just spending money; they are deliberately using some low-tax space.

Now the beginner questions become easier to see:

- How much taxable income did that create?

- Did the withdrawal order keep the Roth account intact?

- If the market falls, do you still have room to adjust next year?

That is the right shape of the problem.

The first year of retirement is not just a spending year. It is a systems test. You are testing whether your account structure, spending level, and withdrawal order work together under real conditions.

If you want a simpler version of this same logic, think of drawdown as answering one question at a time:

- Which account can I spend from most easily?

- Which account should I protect for later?

- Which withdrawal creates the least future tax trouble?

If you can answer those three questions clearly, you are already ahead of most retirees.

What beginners should not do

There are a few traps worth avoiding early.

1. Do not assume one withdrawal rule fits everyone

Your account mix matters.

A household with mostly taxable assets has a different problem than a household with mostly traditional IRA money. A household with strong Roth balances has more flexibility than a household with no Roth assets at all.

2. Do not ignore future tax pressure

A low-tax early retirement year can look good on paper while setting up a much larger future tax bill.

That is why a simple “take taxable first and forget everything else” rule can become expensive later.

3. Do not treat retirement like a static monthly bill

Retirement is not the same as a paycheck replacement spreadsheet.

Healthcare, taxes, travel, helping family, and market volatility all change the picture. Spending is not one flat line forever.

4. Do not assume the first plan is the final plan

The point of a beginner drawdown plan is to create a stable base.

You are not trying to engineer the perfect solution on day one. You are trying to avoid obvious mistakes while preserving flexibility for better decisions later.

A cleaner mental model for beginners

If you want one sentence to hold onto, make it this:

Drawdown is the art of choosing which dollars to spend now so the rest of your money can last longer, be taxed less, and remain more flexible later.

That means the order matters.

It means taxes matter.

It means the first few retirement years matter more than most people realize.

And it means the beginning of your retirement plan should be simple enough to follow under stress.

What comes next

This article is the foundation.

In Part 2, we will compare the main drawdown strategies — sequential, blended, and cyclical — and look at when a simple order of operations is enough and when a more tax-aware approach may fit better.

In Part 3, we will go deeper into the advanced FI planning layer: Roth conversions, RMD suppression, account location, healthcare planning, and the tax mechanics that shape the long game. RMDs, or required minimum distributions, are forced taxable withdrawals from certain retirement accounts later in life — and they are one reason early tax planning can matter.

A soft next step

If you are still building toward FI, the drawdown phase is easier to plan when the accumulation phase is already visible. FI Architect for iOS can help you model income, expenses, investments, taxes, inflation, and retirement assumptions so you can see how your FI timeline changes as life changes.

You do not need a perfect drawdown plan today. Start by making the path visible.

Sources and further reading

- BiggerPockets Money Podcast — The Ultimate Guide to Early Retirement Drawdown (2026)

- BiggerPockets Money Podcast — The Four Fundamentals of Retirement Drawdown

- ChooseFI — Safe Withdrawal Rates, Drawdown Strategies, RMDs and 50 Year FI Timelines

- Fidelity — Savvy tax withdrawals

- Charles Schwab — What Is Sequence-of-Returns Risk?

- Mad Fientist — How to Access Retirement Funds Early

- Early Retirement Now — The Safe Withdrawal Rate Series

Disclosure

This article references concepts discussed on BiggerPockets Money, ChooseFI, and other public retirement-planning sources. NJL Design Lab is not affiliated with, endorsed by, or sponsored by those podcasts or their creators. Any podcast names are used solely for nominative fair use purposes to identify the source of the ideas being discussed.