Part 3: Advanced FI Planning: Roth Conversions, RMD Suppression, and the Tax Mechanics of Retirement

After exploring foundational and intermediate drawdown strategies in Part 1 and Part 2, this final article builds the advanced layer: integrating Roth conversions, RMD suppression, and tax-efficient flexibility across decades.

Now the focus shifts from which account to draw from to how to engineer a multi-decade tax-efficient retirement planning system that stays flexible under changing tax, healthcare, and estate conditions.

Here the question is no longer just which account should I spend first? The question becomes: How do I design retirement income so it stays tax-efficient, flexible, and resilient over decades?

That means Roth conversions, future RMD pressure, account location, healthcare, Social Security timing, and estate outcomes all belong in the same conversation.

Current-law caveats

This article is a planning framework, not tax advice. The rules below are current-law concepts that can change.

- RMDs: under current federal law, RMDs generally begin at age 73 for many retirees, with SECURE 2.0 moving the age to 75 for later birth cohorts. Verify the year you turn 73/75 and the applicable birth-cohort rule before relying on any withdrawal schedule.

- Roth conversions: a conversion is not the same thing as instant penalty-free access. Roth rules include five-year clocks, ordering rules, and age-based distribution rules that matter for planning.

- ACA / IRMAA: healthcare premiums and subsidies depend on current law, income thresholds, filing status, and the specific year’s premium-credit rules.

- Estate planning: inherited-account treatment varies by account type, heir type, beneficiary design, state law, and future tax law.

- State taxes: always test the plan against both federal and state rules when applicable.

Why advanced FI planning matters

A retirement portfolio is not just a balance sheet.

It is a tax engine.

It is a healthcare input.

It is an estate plan.

And for early retirees, it can also be a decades-long control problem.

If you only optimize for the first year of retirement, you can make the rest of the plan worse.

That is why advanced drawdown planning starts with the long view.

Roth conversions and the break-even tax question

One of the most important advanced tools is the Roth conversion.

You move money from a traditional account into a Roth account, pay tax now, and potentially create future qualified withdrawals that are tax-free.

That sounds simple. The real question is whether the conversion is worth it.

The break-even idea

The core decision is this:

What future tax rate makes the conversion worth doing today?

This is the logic behind the break-even tax rate.

If your future tax rate is likely to be higher, a conversion tends to look more attractive.

If your future tax rate is likely to be lower, the answer is less obvious.

For example, if converting $50,000 today pushes you into a 22% bracket but your projected RMD-era rate is 28%, the conversion may create long-run savings. The math works because you are deliberately paying tax in a lower bracket today to avoid having more of that same capital taxed at a higher bracket later.

But the analysis is more nuanced than a simple current-vs-future tax comparison because conversion taxes, growth, basis, and available taxable funds all affect the result.

Why taxable funds matter

A conversion is often most attractive when you can pay the tax from a taxable account instead of withholding from the converted amount.

That keeps more money inside the tax-advantaged system and preserves the full conversion value.

The early-retirement conversion window

Early retirement often creates a window where taxable income is lower:

- no salary

- no large bonus

- no Social Security yet

- often more room in lower brackets

Those are the years when conversions may be most useful.

But they should be evaluated intentionally, not done mechanically. A good conversion decision should account for federal tax, state tax, healthcare effects, five-year-rule timing, and how the tax bill will be paid.

The pro-rata trap

This is where it is easy to mix together different Roth strategies.

A Roth conversion is part of the drawdown and tax-engineering conversation: you are moving existing pre-tax retirement money into a Roth account and choosing whether paying tax now improves the long-term plan.

A Backdoor Roth IRA or Mega Backdoor Roth is different. Those are contribution strategies that may help high-income earners build Roth assets before or during the transition to FI. They can be useful, but they are not the same as a retirement drawdown plan.

The caution is the pro-rata rule. Existing pre-tax IRA balances can make a Backdoor Roth conversion partly taxable, which means the strategy needs to be checked before assuming it is clean or tax-free.

Now that we have covered conversions, the next question is what those conversions are trying to prevent.

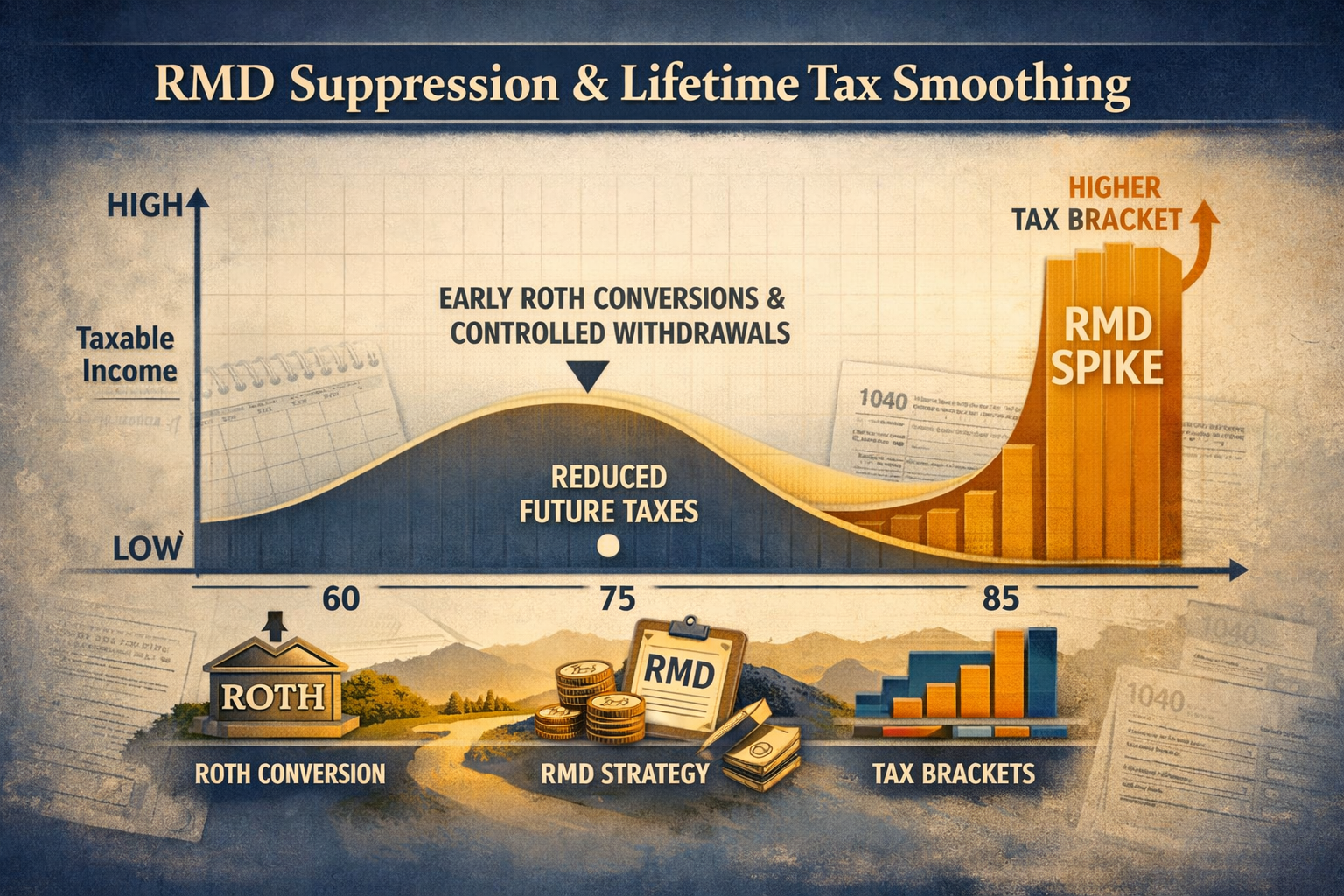

RMD suppression and bracket engineering

Traditional retirement accounts are useful, but they can become a problem if they grow too large.

Why?

Because required minimum distributions do not care about your spending preference. They create forced taxable income later. For example, a household with a large traditional IRA may be forced into higher taxable income once RMDs begin, even if their spending needs have not changed.

The advanced idea

Instead of waiting until RMDs arrive, some retirees deliberately draw down pre-tax accounts earlier.

The goal is not to empty the account.

The goal is to reduce future forced distributions and spread taxable income more evenly across retirement.

That can create several benefits:

- lower future tax spikes

- more control over taxable income later

- more room for Roth conversions in low-income years

- a better inheritance profile for heirs

The tradeoff

This strategy is not free.

If you draw more from pre-tax accounts now, you may pay more tax now.

The question is whether paying some tax earlier reduces a larger tax bill later.

That is the essence of bracket engineering. The chart below shows how earlier Roth conversions and controlled withdrawals can smooth lifetime taxable income instead of waiting for a later RMD spike.

Once the income path is visible, the next layer is asset placement.

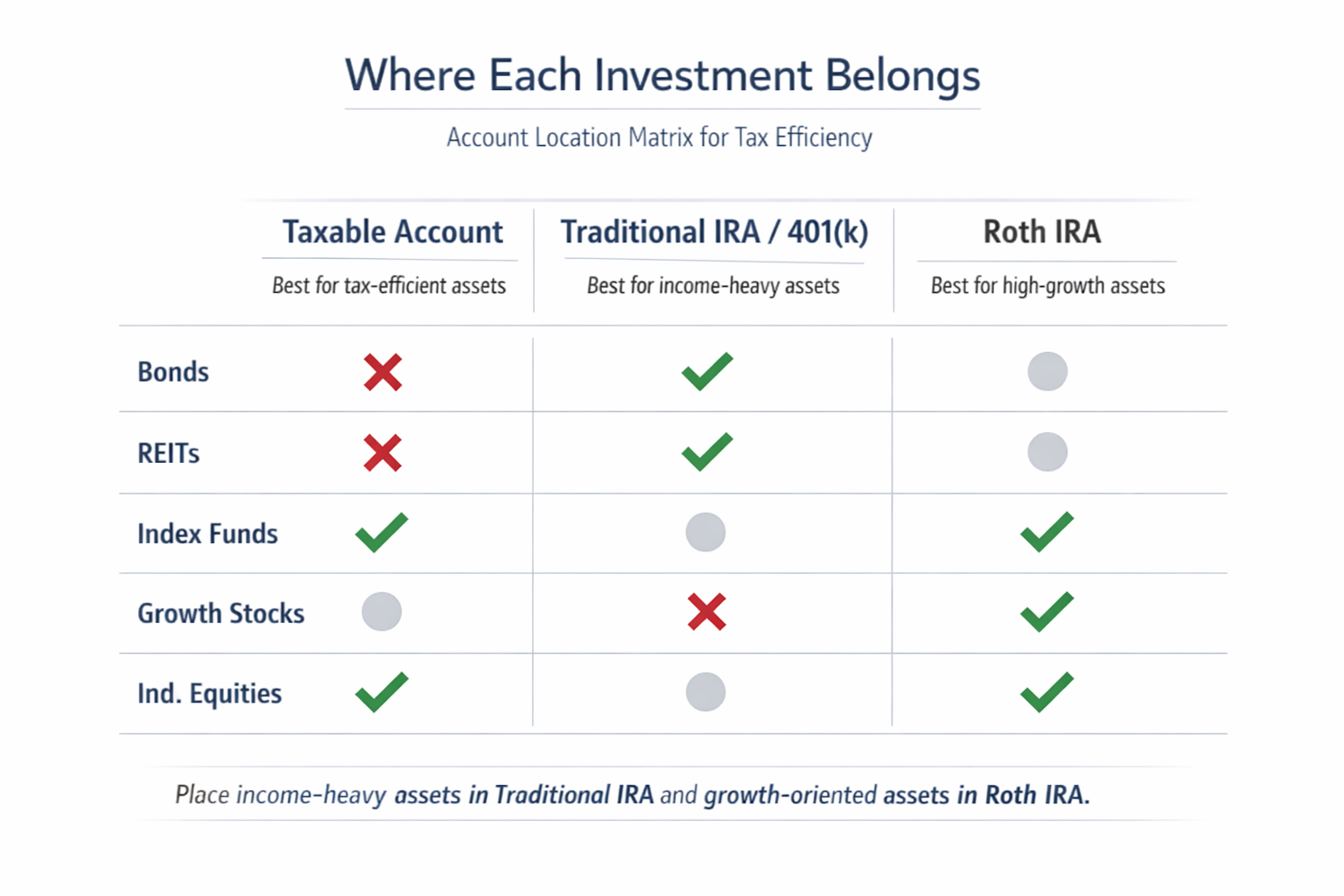

Account location and tax diversification

Advanced retirement planning is not just about withdrawal order.

It is also about where your assets live.

General account-location logic

- Growth-heavy assets often belong where their tax treatment is strongest.

- High-turnover or interest-heavy assets can create drag in taxable accounts.

- Roth accounts are often valuable for the highest-growth assets because future gains can be sheltered.

- Traditional accounts can be useful for assets that would otherwise create a lot of current tax friction.

For example, REITs or bond funds may fit better in traditional accounts when they would otherwise create recurring taxable income, while high-growth equity funds can be especially powerful in Roth accounts if future growth is sheltered. The matrix below is a simplified starting point, not a universal rule.

The right answer depends on portfolio design, but the bigger idea is simple:

The account wrapper matters almost as much as the asset itself.

Why tax diversification matters

A household with only one tax bucket has less flexibility.

A household with taxable, traditional, and Roth assets can choose.

That choice is valuable.

Tax diversification gives you options when tax law, income needs, or market conditions change.

After taxes and account placement, healthcare becomes the next major planning constraint.

Healthcare planning belongs in the drawdown model

Healthcare is one of the biggest reasons retirement planning cannot be reduced to a single withdrawal percentage.

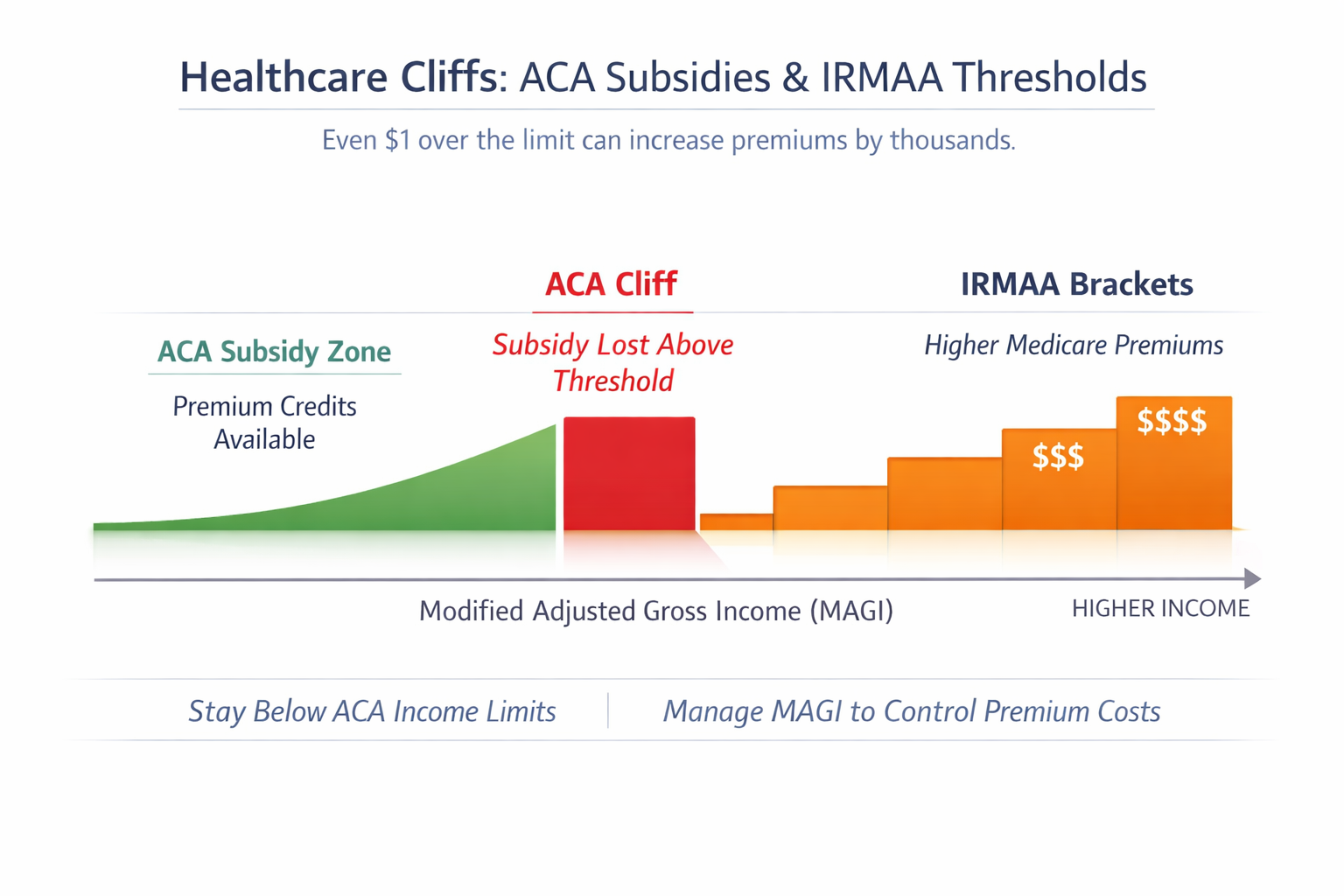

ACA and premium credits

For early retirees, income can affect exchange subsidies.

That means a higher withdrawal in one year can change not just taxes, but healthcare costs too. ACA subsidy planning can be especially sensitive because one extra dollar of income may change premium support under the rules in effect for that year.

So when you compare a sequential strategy to a blended one, you are not just comparing tax outcomes. You are comparing income profiles. The chart below shows how small income changes can trigger large premium jumps — the healthcare cliffs every retiree should plan around.

IRMAA and later-life premiums

Later in retirement, income can also affect Medicare-related costs. IRMAA brackets can create step-up premium effects when income crosses certain thresholds.

That means today’s conversion decision can have downstream effects on future premiums.

The key takeaway:

Retirement income planning is not separated from healthcare planning. It is part of the same system.

The same income-management logic applies when household structure changes.

Social Security timing and survivor planning

Social Security is often treated as a later decision, but it belongs in the drawdown framework early.

Why timing matters

The age at which you claim can change:

- how much income you need from the portfolio

- how much room you have for conversions before benefits begin

- how much taxable income you stack in a given year

Delaying Social Security can create more flexibility in the earlier years, but the right choice depends on the whole household picture.

Why survivor planning matters

A retirement plan should not only work for the first retiree.

It should work for the surviving spouse too.

The widow or widower years can create a different tax profile, a different income need, and a different account draw order.

For example, a surviving spouse may move from married-filing-jointly brackets to single brackets while inheriting the full traditional balance. Joint brackets widen and single brackets narrow, which can increase effective tax rates for survivors unless the household plans for the transition early.

That is why advanced planning is never just about averages.

It is about transitions.

Estate and legacy considerations

Drawdown strategy also changes what you leave behind.

- Roth assets are often more tax-efficient for heirs.

- Traditional assets may create taxable inheritances.

- Taxable assets can receive step-up treatment depending on asset type and applicable rules.

The right withdrawal strategy may therefore be different if your goal includes leaving the most efficient legacy possible.

This is another reason advanced planning is more than a spending calculation.

It is a household-level capital allocation decision.

A practical advanced framework

Use this as an annual review sequence, not a one-time checklist.

If you want a repeatable advanced planning process, start here:

1. Map your current tax buckets

- taxable

- traditional

- Roth

- HSA

2. Estimate future tax pressure

- projected RMDs

- likely bracket exposure

- possible healthcare premium effects

3. Identify low-income windows

- retirement gap years

- pre-Social-Security years

- years with unusually low taxable income

4. Test Roth conversion space

- what can you convert without creating an oversized tax spike?

- where does the break-even logic look strongest?

5. Decide whether to accelerate traditional withdrawals

- do you want to reduce future forced income?

- are you comfortable paying some tax earlier to avoid a larger tax burden later?

6. Include estate and survivor outcomes

- what happens if one spouse dies first?

- which account mix best supports the surviving household?

7. Re-check each year

Use the checklist below to turn the framework into an annual planning rhythm.

Annual advanced-planning checklist

Use this as a repeatable annual workflow:

- Check income and brackets: re-estimate current-year taxable income and retirement tax brackets.

- Confirm RMD timing: verify age rules, upcoming thresholds, and whether any law changes affect required distributions.

- Evaluate Roth conversion space: test bracket room, five-year clocks, pro-rata-rule exposure, and how the tax bill will be paid.

- Model healthcare effects: test ACA subsidy planning and IRMAA brackets if applicable, including the effect of one extra dollar of income on premiums or subsidies.

- Adjust for spending changes: update the withdrawal mix if spending needs changed.

- Review estate and survivor assumptions: update beneficiary design, survivor-tax assumptions, and inheritance effects.

- Revisit account location: adjust asset placement if asset mix, holding period, or tax law has changed.

- Set next-year actions: update the plan before the next withdrawal year begins.

This is not a one-time plan.

Advanced FI planning is a recurring review process.

The advanced rule

The most effective retirement drawdown plan is not the one that minimizes tax in a single year.

It is the one that balances present spending, future tax pressure, healthcare effects, and long-run flexibility.

That is the real advanced game.

Not just spending money.

Spending it in a way that keeps the rest of the plan strong.

Advanced FI planning is not about minimizing taxes once. It is about designing a system that adapts to changing brackets, healthcare rules, and household transitions. The concepts in this article turn that complexity into a repeatable annual rhythm.

Once you understand these mechanics, retirement planning becomes a dynamic system — not a static withdrawal rule.

What this series has covered

- Part 1: the beginner mental model for drawdown

- Part 2: sequential vs blended vs cyclical strategies

- Part 3: Roth conversions, RMD suppression, account location, healthcare, and estate mechanics

In other words: the full tax mechanics of retirement.

Together, the three parts turn drawdown from a vague retirement topic into a practical planning system.

Take the next step

Advanced drawdown planning is not something to hold entirely in your head. If you are building toward FI, FI Architect for iOS can help you model the assumptions that shape the long game: income, expenses, investments, debt, taxes, inflation, retirement timing, and scenario tradeoffs.

It will not replace professional tax advice. But it can make the planning conversation clearer before you make irreversible decisions.

- Explore FI Architect for iOS

- Back to Part 2: Sequential vs. Blended vs. Cyclical Drawdown

- Start from Part 1: The Beginner’s Guide to Early Retirement Drawdown

Sources and further reading

- BiggerPockets Money Podcast — The Ultimate Guide to Early Retirement Drawdown (2026)

- BiggerPockets Money Podcast — The Case for Blended (Instead of Sequential) Drawdown for Early Retirees

- BiggerPockets Money Podcast — The Four Fundamentals of Retirement Drawdown

- BiggerPockets Money Podcast — Reach Financial Independence Faster: Backdoor & Mega Backdoor Roth Explained

- ChooseFI — Safe Withdrawal Rates, Drawdown Strategies, RMDs and 50 Year FI Timelines

- Mad Fientist — How to Access Retirement Funds Early

- Early Retirement Now — The Safe Withdrawal Rate Series

- Vanguard — A “BETR” approach to Roth conversions

- AICPA & CIMA — Tax-Efficient Draw Down Strategies

- Journal of Accountancy — Tax-efficient drawdown strategies in retirement

- Fidelity — Savvy tax withdrawals

- T. Rowe Price — Tax-efficient retirement withdrawal strategies

- Charles Schwab — What Is Sequence-of-Returns Risk?

Disclosure

This article references concepts discussed on BiggerPockets Money, ChooseFI, Fidelity, T. Rowe Price, Vanguard, AICPA, and other public retirement-planning sources. NJL Design Lab is not affiliated with, endorsed by, or sponsored by those publications or their creators. Any podcast or brand names are used solely for nominative fair use purposes to identify the source of the ideas being discussed.