Options Greeks 201: Delta, Theta, and IV Before You Sell Premium

If you already understand the basic mechanics of an options contract, the next question is not “what is a call or put?”

The better question is this: what changes the meaning of a short-premium trade once you actually put money at risk?

That is where delta, theta, and implied volatility matter.

A premium number by itself does not tell you enough. It does not tell you how directional the trade is. It does not tell you how fast time decay may work for or against you.

It also does not tell you whether the premium is high because the market is offering opportunity or because the market is pricing in real risk.

If you are selling premium, those three inputs change the conversation.

- Delta tells you how much directional exposure you are taking on.

- Theta tells you how time is changing the trade.

- Implied volatility tells you what kind of premium context you are stepping into.

That is the mental model.

This is not a 101 primer on how options work. Assume you already know the basics. The point here is to help you read the trade more clearly before you sell it.

Why Greeks matter once you already know the basics

The Greeks are not a guarantee of what will happen. They are theoretical guideposts for how an option may behave if the underlying changes, time passes, or volatility shifts.

That matters because a short-premium trade is not just “collect premium and wait.” It is a bundle of exposures:

- directional exposure

- time decay

- volatility risk

- assignment risk

If you ignore those layers, you may end up choosing a strike for the wrong reason. For example, you may chase a larger credit without realizing you also took on more downside exposure. Or you may focus on delta alone and ignore the volatility environment that is making the premium look unusually attractive.

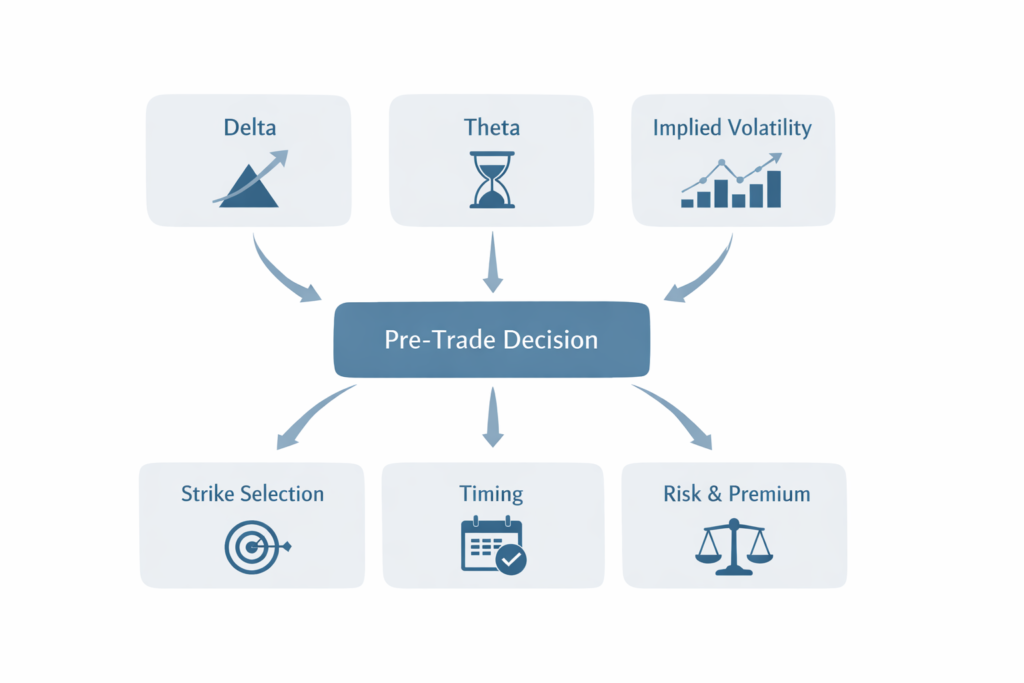

A better approach is to ask what each Greek is telling you before you enter the trade.

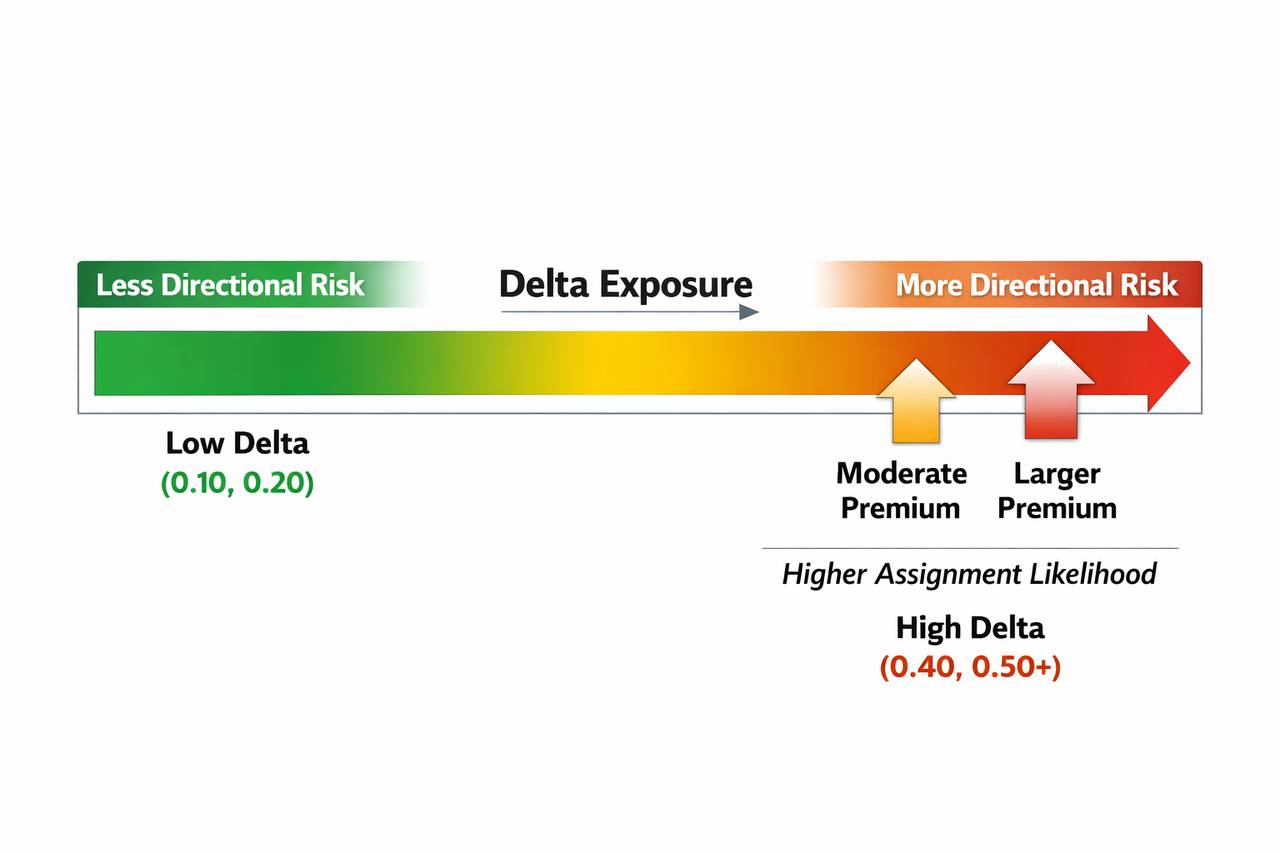

Delta tells you how directional the trade really is

What it measures

Delta is the first filter many short-premium traders look at. In plain language, it is a theoretical estimate of how much an option’s premium may change for a $1 move in the underlying.

It is also often used as a rough intuition for the chance of ending in the money, but that is still only a heuristic. That last part matters.

How it changes the trade

Delta is useful, but it is not a promise. A short put with a lower absolute delta is not “safe.” It is simply less directionally exposed than a higher-delta alternative, assuming everything else is comparable.

- Lower delta usually means less directional exposure and less premium.

- Higher delta usually means more directional exposure and more premium.

- A changing delta can make a trade feel very different after the underlying moves.

One action to take

Use delta to compare strikes with different levels of directional exposure. Ask whether assignment would still fit your plan before the trade is on.

If you sell a short put with a delta around 0.20, you are usually taking less directional risk than if you sell one with a delta around 0.40. But the lower-delta strike also tends to bring in less premium.

What could go wrong: you treat a low delta as “safe,” then a sharp move pushes the strike much closer to the money than your original snapshot implied.

So the question is not “what delta is best?” The question is: what delta matches the trade I actually want to own?

Once you understand how directional the trade is, the next question is how time will change that exposure.

Theta is the clock working for or against you

What it measures

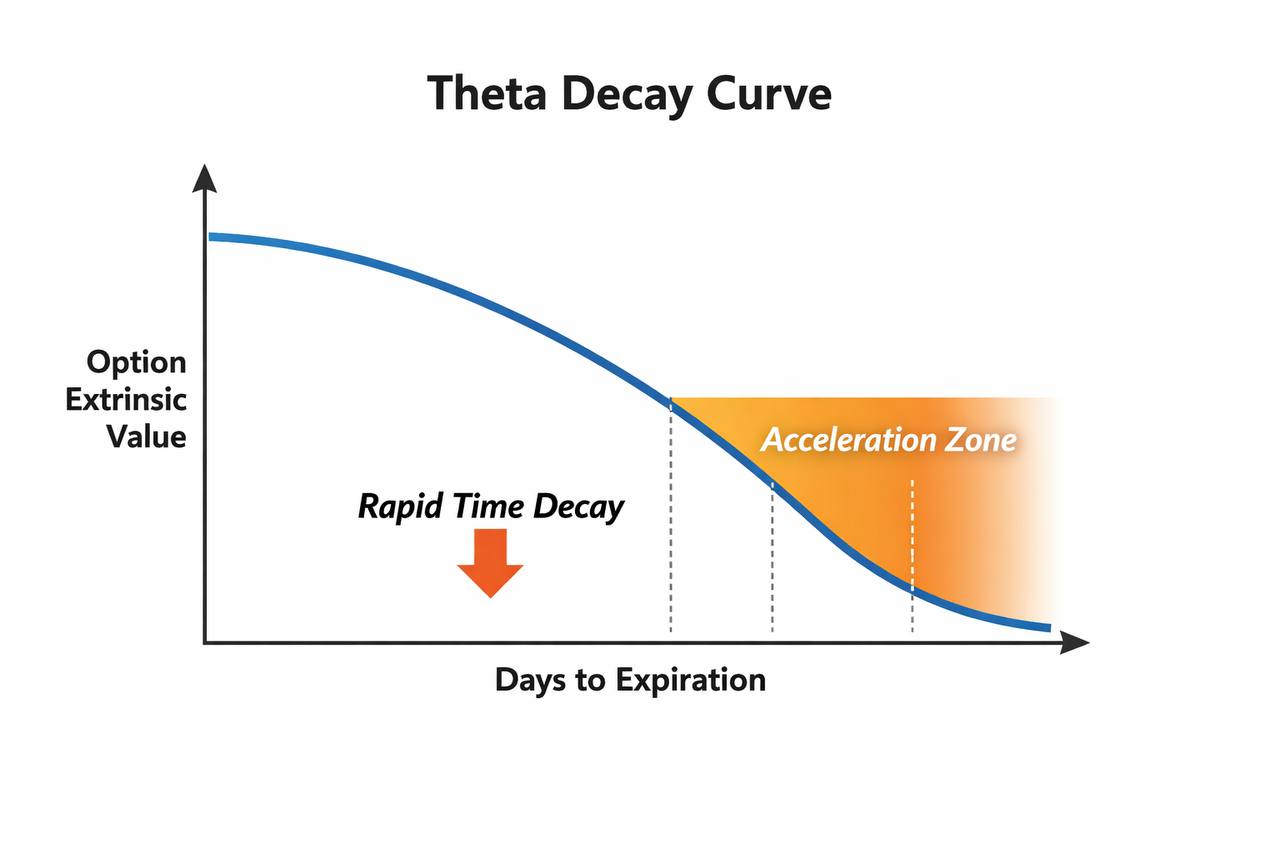

Theta measures time decay: the way an option’s value may decline as expiration gets closer. Theta is not a reward — it is simply the mathematical decay of optionality.

How it changes the trade

Theta is not linear. It does not decay in a neat straight line. Time decay tends to accelerate as expiration approaches, which means the trade can feel very different in the final stretch than it did when you first opened it.

- early in the trade, decay may feel manageable

- late in the trade, decay can speed up

- near expiration, price moves can matter more than traders expect

One action to take

Decide before entry whether you are willing to hold into the final days. For sellers, theta can be a tailwind if the underlying stays within your expected range, but it does not remove risk.

What could go wrong: you focus on daily decay while a sudden move in the underlying overwhelms several days of theta in one session.

That last part is where a lot of confidence gets tested.

The closer you get to expiration, the more you need to understand what can still go wrong.

Implied volatility is the context around the premium

What it measures

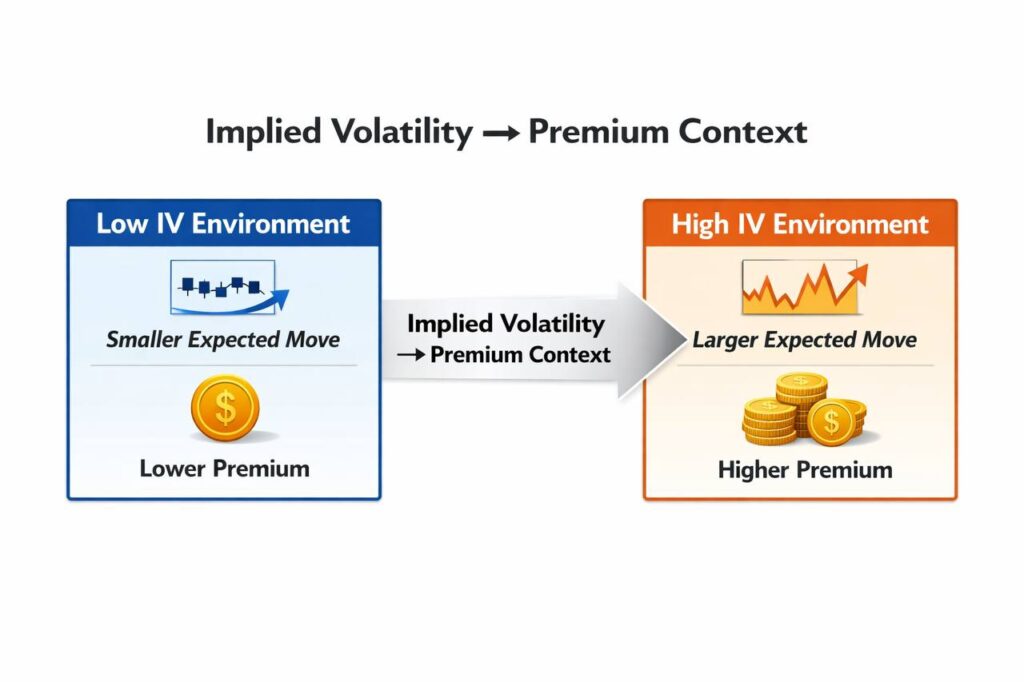

Implied volatility is the market’s expectation of future movement, expressed through option pricing. It is different from historical volatility, which is backward-looking.

Many traders use IV rank or percentile to compare today’s volatility to its recent history, but those are context tools — not guarantees.

How it changes the trade

Implied volatility is where many traders make their biggest mistake. They see a rich premium and assume the market is handing them a gift.

That is not what is happening. If implied volatility is elevated, the premium may look attractive, but it is often elevated for a reason.

- earnings

- a product event

- macro risk

- sector uncertainty

- a broader jump in expected movement

One action to take

Ask why the premium is rich before you sell it. Are you being paid more because the market is giving you an opportunity, or because the market is warning you about risk?

What could go wrong: you sell premium before a known event, get the direction roughly right, and still underestimate how violently the underlying can move.

Premium is not free money. It is compensation for taking risk.

That distinction matters.

When Greeks can mislead you

The Greeks are useful because they make risk more legible. They become dangerous when you treat them as fixed truths.

Model limit: Greeks assume “all else equal,” which is rarely how real markets behave.

Model limits

- Delta can change quickly during large price moves or volatility shocks.

- Theta can accelerate near expiration, but sharp price moves can overwhelm decay.

- Implied volatility can stay elevated longer than expected.

- A volatility crush can change option prices even when direction is roughly right.

Use the Greeks as a dashboard, not as permission to ignore the road.

Assignment awareness is where theory becomes real

Once you sell premium, assignment is no longer an abstract concept.

Assignment is not failure — it is the contract doing exactly what it was designed to do. If your short option is assigned, you have an obligation to do what the contract requires. That is part of the trade, not a surprise outcome.

This is where the Greeks become practical instead of theoretical.

- Delta helps you think about how likely the trade is to move toward the strike.

- Theta helps you understand how much time is left for the market to work in your favor.

- Implied volatility helps you understand whether the premium is rich because the market expects bigger moves.

Put together, those inputs help you judge whether the strike you chose actually fits your plan.

That is especially important for short puts and covered calls, where the trade is often framed as “premium income.” The phrase can make the trade sound simpler than it is. In reality, you are choosing a strike, taking on a risk profile, and deciding in advance how you will respond if the trade moves against you.

The best time to think about assignment is before entry.

A practical example: reading the trade as a whole

Imagine a stock trading at 100.

You are thinking about selling a put with a 95 strike and about 30 days to expiration.

Suppose the put pays a $2.00 premium. If assigned, your effective purchase price would be about $93 before commissions and fees: the $95 strike minus the $2 premium received.

That makes the tradeoff more concrete. You are not just “collecting $2.” You are accepting the possibility of owning the stock around $93 while still carrying downside risk below that level.

If implied volatility or delta were higher, the premium might be larger, but the market would also be signaling more expected movement or a greater chance of assignment.

Here is what the Greeks are telling you:

- Delta: the trade has some directional exposure, but not as much as a higher-strike put would.

- Theta: time decay is working in your favor, but the pace of that decay may change as expiration gets closer.

- Implied volatility: if IV is elevated, the premium may be richer, but the market is also pricing in a larger expected move.

Now ask the real questions:

- Would you still want the stock at the effective price if assigned?

- Is the premium worth the downside exposure?

- Is the higher premium coming from opportunity, or from a known event risk?

- If the trade moves against you, what is your plan before the trade opens?

That is the point of using the Greeks together. They do not predict the future perfectly. They help you understand what kind of trade you are actually making.

Pre-trade checklist: before you sell premium, check these four things

- Delta: Know how directional the strike is before you choose it.

- How directional is this strike?

- Am I comfortable with that amount of exposure?

- Theta: Decide how long you are willing to hold the trade.

- How does time decay behave on this trade?

- Am I prepared for the final days before expiration?

- Implied volatility: Know why the premium is rich before treating it as attractive.

- Is the premium high because the market expects a bigger move?

- Do I understand why the premium looks rich?

- Assignment: Treat assignment as a planned outcome, not a surprise.

- What happens if I get assigned?

- Do I have a plan before the trade opens?

If those answers are vague, the trade is probably not ready.

Common mistakes traders make with the Greeks

Treating delta like a guarantee

Delta is a heuristic, not a promise.

Thinking theta means “easy profit”

Time decay helps, but it does not eliminate downside risk.

Chasing premium without asking why IV is high

Elevated premium often reflects elevated risk.

Ignoring assignment until it happens

Assignment is part of the trade structure, not an edge-case surprise.

Making the trade too complicated

You do not need a perfect model. You do need a clear understanding of what you are taking on.

FAQ

Is delta the same thing as probability?

No. It is sometimes used as a rough proxy for probability of finishing in the money, but that is only a shortcut. Delta is still a theoretical sensitivity measure, not a certainty.

Does theta mean a short option will profit if I wait long enough?

No. Time decay can help a short-premium position, but price moves and volatility changes can still create losses.

Should I only sell premium when implied volatility is high?

Not necessarily. Higher IV can mean richer premium, but it can also mean higher expected movement. The key is understanding why IV is elevated.

Do the Greeks tell me exactly what will happen?

No. They help you understand the trade’s exposure. They do not guarantee the result.

Go deeper

If you want the contract mechanics before the Greek-level view, start with Options Trading 101: What Beginners Need to Know Before Selling a Put.

For the official risk disclosure that options traders are expected to understand, review the OCC’s Characteristics and Risks of Standardized Options.

This article is for educational purposes only and is not investment advice. Options involve risk and are not suitable for all investors.

Options are not about predicting every move correctly. They are about understanding what you are exposed to before you enter the trade.

When you read delta, theta, and implied volatility together, you make the trade more legible. That does not remove risk. It gives you a better way to choose strikes, set expectations, and think ahead about assignment.